The global Islamic finance market: part 1, Sukuk bonds

The Islamic Finance market is a dynamic and growing global financial market. Within that market, Sukuk bonds are a major sector, showing continuous growth and development in recent years.

Sukuk bonds are similar to conventional corporate bonds in terms of the parties involved and the purpose of the bond issuance, ie raising finance. However, there are certain key structural differences based on the underlying approach that a Sukuk bond is an economic and equitable joint venture between the issuer and the investors (Sukuk bondholders). This means that the assets acquired by the Sukuk bond issuance will be jointly owned and managed to generate profits, which are then used to repay the participating bondholders. Hence, unlike conventional bonds, the Sukuk bondholder does not receive interest, but instead receives a portion of the profits derived from the revenues generated by the asset acquired with the proceeds of by the Sukuk bond issuance.

The Accounting and Auditing Organisation for Islamic Financial Institutions (AAOIFI) issues standards for accounting, auditing, governance, ethical and Shari'ah compliance. It has defined a number of different types of Sukuk bonds, including those issued by sovereigns, quasi-sovereigns, supranationals and corporates, as well as “green” Sukuk bonds, each of which employs slightly different structures.

Regardless of the Sukuk structure chosen, most issuers will incorporate an independent, bankruptcy remote SPV and transfer title of the acquired assets to the SPV.

The jurisdiction of the SPV will determine the regulatory financial authority which will be tasked with ensuring that adequate protections are in place to protect the Sukuk bondholders. To ensure investor protection, regulators require the selection of a Sukuk trustee, security trustee, murabaha agent, investment agent and other corporate service providers. Regulatory requirements cover financial and reporting obligations of the SPV, as well as protection of the revenue streams generated by the underlying Sukuk assets.

The global Sukuk bond market has proven to be popular with a wide range of participants. From a social and ethical point of view, Sukuk finance is a desirable solution for large-scale projects, avoiding interest debt (“Riba”) that is prohibited under Islamic law. Various sovereign and quasi-sovereign countries have been able to fund major projects having a direct and positive impact on communities and the economies of Shari’ah law-compliant countries. As a result, Sukuk bonds are recognised and accepted as a more “ethical” way of raising finance, with a positive impact on society, which is also consistent with the increasing adoption of ESG investing.

These and other positive attributes of Sukuk bonds have also attracted the corporate sector. The increased participation of the corporate sector year-on-year illustrates the increased popularity of Sukuks among corporate investors. Considering that the investor base comprising of Shari’ah compliant investors is largely untapped, this represents a huge opportunity for the global Islamic capital markets.

Sukuk bonds are also becoming more and more popular geographically. The main participants include the Middle East, Africa, Europe and Asia, as well as areas with large Muslim populations such as Malaysia, Saudi Arabia, Dubai, Indonesia and Turkey.

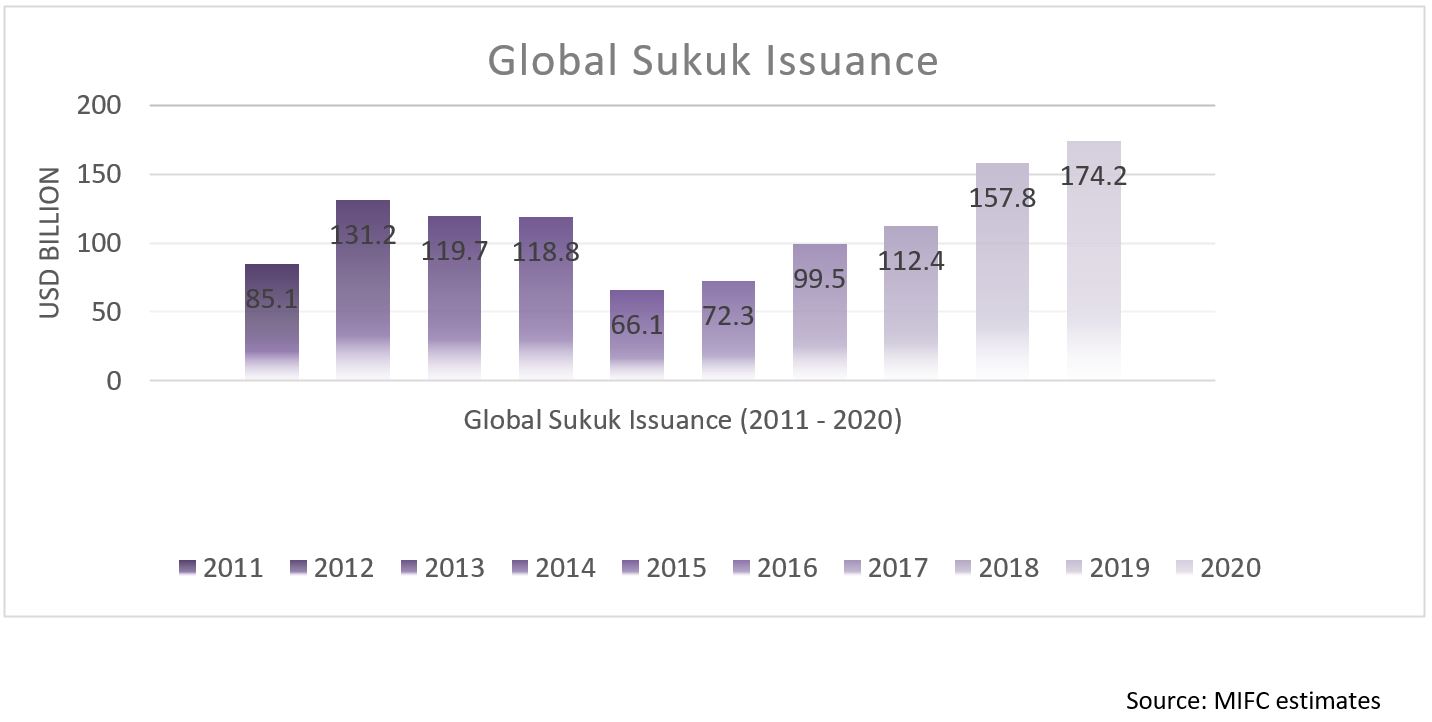

In addition, London has developed into an important location for the Islamic finance industry. There is a sizeable number of Islamic financial services providers, Shari’ah-compliant banks and Sukuks listed on the London Stock Exchange. This makes the UK a very attractive proposition in terms of regulatory framework and tax systems for Islamic finance participants who may be better served from this geographical location. For example, from 2019-2020, the Sukuk market saw an increase of 16.5%, peaking in 2020, when the market hit a new record US $174.2 billion in total issuances, compared to US $157.8 billion of total issuances in 2019.

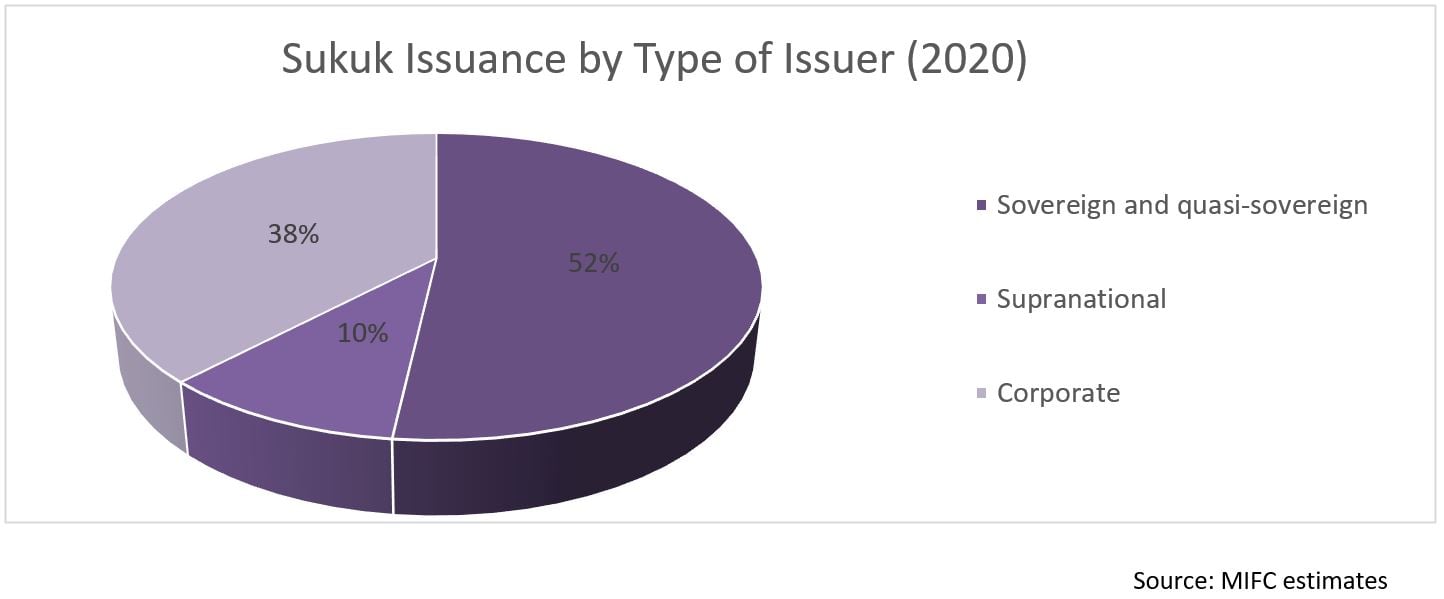

In 2020 global Sukuk issuances were largely comprised of sovereign, quasi-sovereign and supranational issuances, representing 62.1% of all issuances. The remaining 37.9% represents the growing participation of corporates and multinationals in this sector.

How can TMF help?

Sukuk bond issuances are regulated and require experienced service providers to act in several roles. As Sukuk issuances continue to increase with sovereign and corporate issuers, TMF Group is ideally placed to assist with any administrative challenges to ensure a smooth and successful issuance.

Our capital markets group has dedicated teams of experts located in London, Dubai and Malaysia. Our capabilities include providing regulated services for the full range of Sukuk bond structures, including Sukuk trustee, security trustee, document review, ongoing transaction support, bespoke monitoring, or tailored accounting and reporting requirements. Contact us.