Driving finance transformation: the pros and cons of shared service centres for finance and accounting

Is setting up a shared service centre the right move for your company? Financial shared services are widely used by organisations looking to centralise finance and accounting activities, standardise processes and improve control across multiple entities. Typically delivered through a shared service centre or a shared service provider, this model aims to balance efficiency, cost and compliance and is often a key enabler of broader finance transformation initiatives.

A shared service centre (SSC) is a centralised function that delivers core business services for multiple divisions, subsidiaries or regions. In finance, SSCs typically manage high-volume repetitive tasks, such as accounts payable, payroll and financial reporting. Centralising these processes helps reduce duplication, improve consistency and build specialised capabilities within one focused team.

Finance transformation is becoming a core reason that organisations revisit their shared service strategy. Rather than simply centralising transactional work, many companies use SSCs as a platform to redesign finance end to end – standardising processes, embedding automation and improving data quality so that reporting and decision-making become faster and more insight-driven. In this model, the SSC can act as the engine room for scaling capabilities such as process automation, real-time reporting and AI-enabled forecasting, while freeing business-facing finance teams to focus on partnering and value creation.

Companies typically consider finance and accounting shared services for four key reasons:

- Process standardisation and efficiency

Standardised processes make it easier to design and maintain a strong control environment; input and output reports become consistent, review cycles are shortened and rework is reduced - Enabling finance transformation

Beyond efficiency, SSCs are often used to modernise finance end to end by standardising data and processes, embedding automation and creating a foundation for faster reporting, better forecasting and more value-added business partnering - Cost savings

Automation and process optimisation within a shared service centre can significantly reduce operating costs, particularly for transactional accounting activities - Better business insight

Decentralised finance teams often spend considerable time collecting data rather than analysing it – centralisation enables faster access to management information that is timely, comparable and decision‑relevant

Pros and cons of finance and accounting shared services

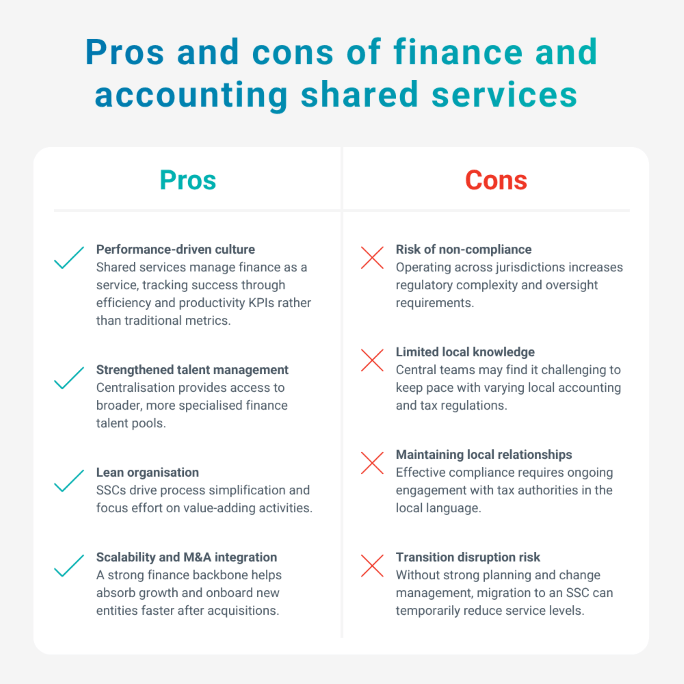

Pros of finance and accounting shared services

1. Building a performance-driven culture

Most companies don’t use KPIs to monitor the activities of internal finance and accounting functions. Those that do tend to focus on traditional, outward-looking KPIs including AR (accounts receivable) days and AP (accounts payable) days. This approach changes significantly within SSCs: finance and accounting functions are managed as a service, measured from an efficiency and productivity perspective.

Common SSC KPIs include metrics such as number of invoices per FTE (full-time equivalent), FTE cost as a percentage of revenue, error rates, number of manual entries, and so on. Continuous monitoring of these indicators helps organisations identify areas for improvement and opportunities for automation.

2. Strengthening talent management

Finance talent shortages can make recruitment challenging. Centralising finance and accounting functions helps mitigate this by enabling access to broader, more specialised talent pools, often in locations with greater availability of skilled professionals.

3. Developing a lean organisation

SSCs prompt organisations to reassess how work is done and whether certain activities are still required. This often results in a more streamlined operating model focused on efficiency and value-added work.

4. Enabling scalability and faster integration after M&A

A mature SSC makes it easier to scale finance operations without a corresponding increase in headcount. It can also accelerate post-merger integration by providing a standard process backbone for onboarding new entities, harmonising master data and bringing acquired businesses into a consistent close, reporting and control rhythm.

Cons of finance and accounting shared services

1. Risk of non-compliance

Operating across multiple jurisdictions increases compliance complexity. While transactional accounting processes can be centralised, organisations must still meet local tax and reporting requirements. Additional processes – such as data reconciliation oversight and tracking tools – may need to be established and monitored, with specialist support required to address any knowledge gaps.

2. Limited local knowledge

Local accounting and tax rules vary from country to country, with differences in local GAAP, VAT, GST and reporting requirements. Maintaining up-to-date expertise across all jurisdictions can be challenging for a centralised team.

3. Maintaining local relationships

Maintaining regular contact with local tax authorities is an important factor in keeping your operations compliant. Teams must be able to communicate with authorities in the local language and respond promptly to queries. Failure to respond in time and in the right way could lead to fines and penalties.

4. Transition disruption and business continuity risk

During migration to an SSC, service levels can dip while processes, systems and roles are stabilised. Common issues include delayed invoice processing, slower month-end close and increased query volumes, with parallel running and remediation adding cost. Strong transition planning, clear ownership and robust change management are essential to protect business continuity.

Location and operating model considerations

Choosing the right location and operating model is one of the most critical decisions when setting up a financial or accounting SSC. While cost efficiency is often a primary driver, long‑term success depends on a broader set of strategic and operational factors, including location and cultural fit.

Organisations must weigh the trade‑offs between nearshore and offshore models: offshore locations can deliver significant cost savings, whereas nearshore SSCs often offer stronger cultural alignment, language capabilities and time zone coverage.

Location strategy

The location of an SSC has a direct impact on service quality, compliance and scalability. Finance and accounting teams need skilled professionals who understand technical accounting requirements and local statutory, tax and reporting obligations. Talent availability, language capabilities and regulatory environments therefore play a central role in location decisions.

Time zone alignment with key markets, business continuity considerations and the maturity of the local finance ecosystem should also be evaluated. Focusing solely on low-cost geographies can introduce hidden risks, particularly where regulatory complexity or talent scarcity affects accuracy and timeliness.

Operating model options

There is no one-size-fits-all model for shared services. Organisations typically choose between three main approaches:

- Captive (in-house) shared service centre: offers greater control but often requires significant upfront investment and long-term management commitment

- Hybrid models: combine internal shared services with specialist third‑party support for specific countries, jurisdictions or activities

- Fully outsourced shared service provider models: allow organisations to scale more quickly and access deep local expertise, while reducing operational complexity

Each model offers a unique balance of cost, control and speed to value. The right choice depends on organisational maturity, geographic footprint and risk appetite.

Standardisation versus local requirements

A common challenge in shared service environments is balancing global standardisation with local accounting, tax and reporting requirements. Effective models allow for necessary local nuance to avoid compliance gaps, rework and delays.

Governance and accountability

Strong governance is critical to shared service success, with clear ownership, defined service levels and effective escalation needed to manage performance. Without this foundation, consistent outcomes are difficult to achieve.

5 considerations for managing complexity in a shared service environment

Managing financial and regulatory complexity is one of the biggest challenges in shared service environments. Differences in local reporting, tax rules and regulatory expectations can undermine standardisation if they are not actively governed.

Here are five key considerations for managing compliance and complexity in a shared service environment:

1. Navigating multi‑jurisdiction compliance

Financial and accounting shared services must operate within a landscape of diverse accounting standards, statutory reporting rules and tax regulations. While processing may be centralised, accountability for compliance remains local. This creates a complex operating environment where inconsistencies in interpretation or execution can quickly lead to errors and missed deadlines.

2. Risk and control challenges

Centralised models can amplify risk if controls are not designed with local requirements in mind. Common challenges include inconsistent application of local regulations, weak audit trails and insufficient oversight of in-country filings. As shared service centres scale, these risks increase unless governance and control frameworks evolve in parallel.

3. Data quality and visibility

Reliable financial reporting depends on consistent, high-quality data. In practice, shared service environments often rely on multiple ERPs, local finance systems and manual workarounds. This fragmentation can reduce visibility, slow reporting cycles and undermine confidence in financial outputs – particularly in statutory and tax reporting.

4. Compliance complexity as a barrier to transformation

When shared service centres spend significant time managing local compliance and administrative coordination, finance transformation initiatives often stall. Country-by-country exceptions (different statutory formats, tax calendars, filing portals and documentation requirements) create manual workarounds that prevent true process standardisation and make automation harder to implement at scale. The knock-on effect is slower close and reporting cycles, inconsistent data and higher rework – which limits the SSC’s ability to shift capacity from transactional delivery into value-adding activities such as analysis, forecasting and business partnering. Reducing compliance friction and designing the SSC with clear ownership, controls and local expertise where needed, is therefore a prerequisite for achieving broader finance transformation goals.

5. The role of specialist partners

Many organisations address these challenges by working with shared service providers that combine centralised execution with deep local compliance expertise. This approach can help reduce risk, improve consistency and provide the scalability required to support growth across multiple jurisdictions, while maintaining confidence in statutory and regulatory outcomes.

Key takeaways

- Well-designed SSCs can act as a platform for finance transformation by enabling standardisation, automation and more insight-driven reporting

- Finance shared services can improve efficiency, control and scalability when designed correctly

- Accounting shared services require strong governance to manage local compliance risks

- Location and operating model choices directly influence cost, speed to value and cultural alignment

- The right SSC model depends on jurisdictional complexity, talent availability and regulatory requirements

- Strong governance and local expertise are essential to manage compliance and complexity across jurisdictions

Talk to us

Our in-country specialists help organisations balance standardisation with local compliance requirements across jurisdictions.

Speak to our experts to explore how we can support and optimise your finance shared services model.