Sweden’s tax environment: an overview

Sweden’s tax environment remains a model of transparency, efficiency and investor-friendly regulations in 2025. With the corporate tax rate now at 20.6%, generous exemptions for holding companies and a trusted tax authority in Skatteverket, Sweden offers a stable and predictable tax framework for international businesses and residents alike.

Recent tax reforms in Sweden – aimed at curbing aggressive tax planning and aligning with global standards – further reinforce the country’s commitment to fair and transparent taxation. Among these are new rules to restrict the deduction of interest expenses to a maximum deductible net interest income of 30% of EBITDA for companies with a net interest income of more than SEK5mn.

For companies looking to expand or streamline operations in the Nordics, understanding taxes in Sweden is not just beneficial – it’s essential.

Overview of Swedish taxes

Sweden maintains a transparent and efficient tax system, designed to support its robust public services and social welfare infrastructure. The corporate tax rate in Sweden is a competitive 20.6%.

Standard VAT in Sweden is 25%, with reduced rates of 12% and 6% for specific goods and services. Social security contributions are substantial and primarily funded by employers, covering pensions, health insurance and other benefits.

Sweden is especially favorable for holding companies, subsidiaries and branch offices, as it offers generous exemptions on capital gains and intra-group dividends. The country also has over 90 tax treaties to prevent double taxation and facilitate international business.

Other key attributes of the Swedish tax environment include:

- No thin-capitalisation rules

- No withholding tax on interest or royalties

- No stamp duty or capital duties on share capital

- Lower tax rate for key foreign employees.

Breakdown of taxes in Sweden

Below are the key Swedish taxes that companies should know.

Corporate income tax (CIT)

Low by international standards, the Swedish CIT rate is currently 20.6%. The effective rate can be even lower if companies choose to make deductible annual appropriations to a tax allocation reserve - known as periodiseringsfond - of up to 25% of their profit. The periodiseringsfond will be taxed after a period of six years. For example, if you contribute to a tax reserve in 2025, it must be reversed by 2031 at the latest, or be offset against losses.

CIT is based solely on a company’s annual profit; no license tax or local corporate tax is payable.

Value added tax (VAT)

VAT in Sweden is 25%. Some goods and services are taxed at a lower rate. For items such as food, hotel accommodation, restaurant and catering services (except for alcoholic drinks), camping and cultural and sporting events, a reduced rate of 12% applies. Newspapers, books, magazines and public transport attract a lower VAT rate of 6%. Services such as medical and dental care, social services, banking and financial services are exempt from VAT.

Capital gains and dividends

Capital gains and dividends from business-related shares are generally exempted from tax. The scope of the exemption is generous compared to other countries. The exemption can apply to shares held in, or dividends received from, Swedish and foreign companies.

Real estate tax

The owner of property or site leasehold in Sweden is liable for real estate tax. The property may be classified as industrial (0.5% real estate tax) or commercial (1% real estate tax).

Withholding tax

Sweden does not levy withholding tax on interest payments, royalties, technical service fees or branch remittance tax. Dividends paid to a non-resident company, however, are subject to 30% withholding tax unless the flat rate is reduced or an exemption applies under a tax treaty or other legislation/regulations.

Corporate tax and employer obligations

There are a number of corporate tax requirements that companies operating in Sweden must adhere to:

Preliminary tax

Companies that are liable for corporate income tax in Sweden must pay preliminary tax during the taxable year. To calculate how much tax is payable, the company must submit a preliminary tax return. The Swedish tax agency then notifies the company of how much tax should be paid each month.

Social security contributions

In 2025, the employer social security contribution rates in Sweden are as follows:

- Pension insurance - 10.21%

- Health insurance – 3.55%

- Unemployment insurance - 2.64%

- Surviving dependants' pension insurance - 0.6%

- Parenthood insurance - 2.6%

- Workplace accident insurance - 0.2%

- General salary tax - 11.62%

The pensionable income is capped at 7.5 times the income base amount, which corresponds to SEK504, 375 for 2025. For the self-employed, however, the total contribution is 28.97% including the same components as those of employer contributions.

Compliance challenges and solutions in Sweden

Companies expanding into Sweden should familiarise themselves with the three most common compliance challenges.

1. Compliance risks not managed properly

Even in a stable regime like Sweden’s, poor tax compliance oversight can have serious consequences. Skatteverket is strict: missing a filing or a required response can trigger penalties immediately. Non-compliance can also lead to fines, reputational damage, or legal issues for executives. Companies must monitor regulations closely and maintain strong internal controls.

2. Excessive time spent on local compliance and coordination

Sweden’s complex local tax and reporting rules are time-consuming. Swedish accounting and tax teams spend nearly half their time on administrative tasks, such as preparing financial statements in Swedish, and working to strict deadlines. Multinational firms must manage multiple advisors across many countries, dealing with language barriers and inconsistent regulations. Many companies are now turning to automation or external partners free up time for planning and analysis.

3. Unbalanced central vs. local involvement

Balancing central oversight with local execution is a common challenge for companies operating in Sweden. If the head office is too disconnected from local tax teams, important decisions may be made without proper visibility. On the other hand, micromanaging every detail can slow things down and limit local expertise. The best approach is to integrate central and local efforts — using clear communication and shared systems. This improves control, avoids inefficiencies and strengthens overall compliance.

4. Practical compliance considerations

While the calendar year applies for personal income tax, the year-end for a company may be fixed at the end of any calendar month (as long as the taxable period comprises 12 calendar months and ends on the last day of a month).

The deadline for submitting tax returns is 1 August. If the fiscal year ends in May or June, the deadline is 15 January of the following year.

All Swedish entities must be registered with the Swedish tax agency for tax purposes. If your business is liable for VAT, you must register for VAT. If you have employees (including yourself if working for a limited liability company), you must register as an employer for pay as you earn (PAYE) tax. Learn more about tax compliance with our statutory accounting services.

K3 and component depreciation for real estate companies

Starting from financial years beginning after 31 December 2025, new accounting rules will impact many companies currently applying the simplified K2 framework. For commercial real estate companies, this often means a mandatory shift to K3 – and with it, the introduction of component depreciation.

If your company owns buildings that generate 75% or more of your total revenue, you’ll likely need to transition from K2 to K3. This includes:

- Property companies leasing out commercial or residential spaces

- Hotels with significant room rental income

- Real estate businesses with substantial rental operations

Under K3, buildings must be broken down into significant components, such as structure, roof, exterior and installations. Each of these is depreciated separately based on its useful life. This approach provides a more accurate reflection of asset value and improves transparency in financial reporting.

For commercial property owners, this means:

- Restructuring your fixed asset register

- Assessing the economic lifespan of each component

- Updating depreciation schedules

- Enhancing clarity in your annual accounts

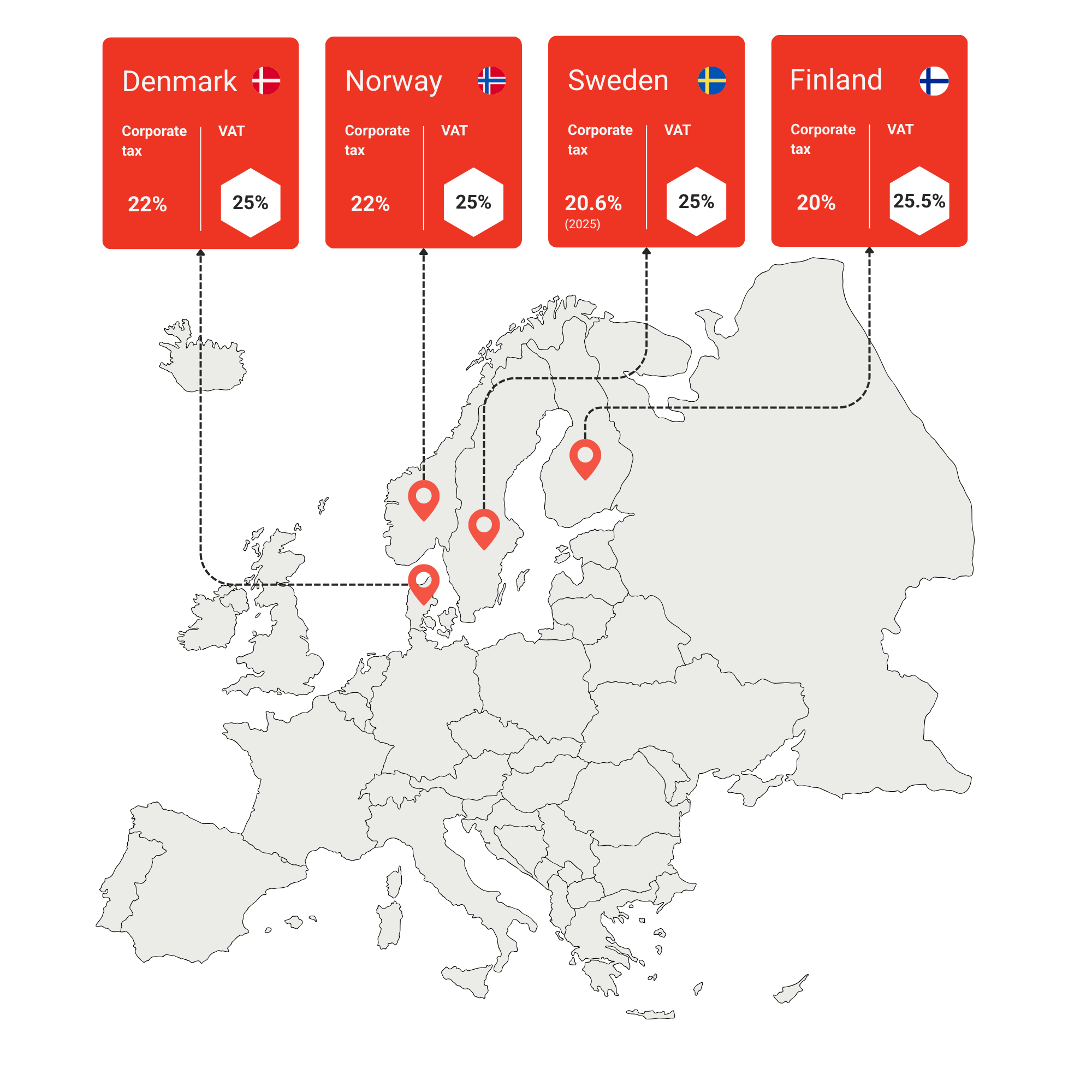

Nordic comparison table

To put Swedish taxes into perspective, it’s helpful to compare them with the country’s Nordic neighbours. While all four countries share a commitment to transparency and strong public services, their tax structures vary in ways that can influence investment and operational decisions.

The table below highlights key differences in corporate tax rates, VAT, social security contributions and capital gains treatment across Sweden, Denmark, Norway and Finland.

Key takeaways

- Sweden offers a competitive and transparent tax environment, with a low corporate tax rate and strong investor protections.

- Capital gains and intra-group dividends are generally tax-exempt, making Sweden attractive for holding companies.

- VAT and social security contributions are significant, and businesses must understand the applicable rates and exemptions.

- Compliance is strict and time-sensitive, with short response windows and penalties for delays or errors.

- Balancing central oversight with local expertise is essential to avoid fragmented compliance and ensure efficiency.

Talk to us

Whether you’re entering the Swedish market for the first time or looking to streamline your existing operations, our local team in Sweden can help.

We specialise in supporting real estate companies through complex accounting changes. Our experts in financial reporting and tax are here to guide you through every step of the K3 transition – from component identification to updated depreciation plans.

Explore how TMF Group can simplify your financial reporting and tax compliance in Sweden, or download our Sweden country profile to learn more about taxes and doing business in Sweden.