Renewable energy in Asia: investment incentives in six key markets

The pace and nuance of regulatory change around renewable energy varies considerably across Asia. Potential investors must understand the position in each jurisdiction. In the second of a two-part series, we examine renewable energy investment incentives in six Asian markets.

Asia is fertile ground for renewable investment, particularly by funds. As we discussed in part one of this series, Asia has a considerable need for renewable energy development, and many countries have committed to ambitious targets around carbon neutrality and the proportion of renewables in their energy mix.

There is also a strong pattern of renewable asset development and a robust pipeline, particularly in relation to solar and, increasingly, wind. This provides an asset pool for funds. It is also too new and impractical a space for investors to access directly, putting funds in a strong position to serve as a useful go-between.

To build the renewable energy assets the continent needs, however, incentives are required to coax private sector capital to participate. Below, we look at the positions of six Asian jurisdictions.

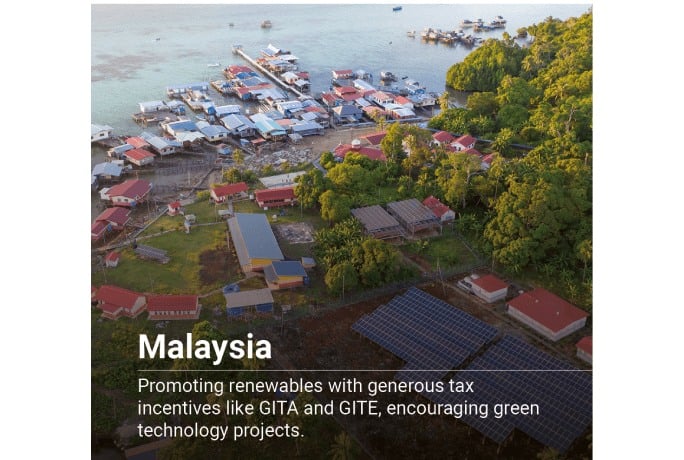

Malaysia

Malaysia’s encouragement of renewables is anchored to a range of green technology tax incentives for service providers and consumers of green technology assets. These break down into two camps: GITA (Green Investment Tax Allowance) on green assets, for owners of these assets and companies that undertake green technology projects; and GITE (Green Income Tax Exemption) for service providers, including a separate category for owners of solar photovoltaic systems.

These schemes are generous: for example, a company granted approval for a GITA asset is eligible for an Investment Tax Allowance which can be offset against 70% of statutory income.

Tax aside, it is also useful to understand the Green Technology Financing Scheme 2.0 (GTFS), which provides financial aid to companies to make it easier for green technology backers to access finance from the private sector. The government guarantees 60% of the loan amount and provides a 2% rebate on the interest or profit rate charged. Profit rate is a term from Islamic finance and is the Shariah equivalent of interest. Islamic finance is more closely entwined with Malaysian banking and investment than it is with any other banking system in the region.

An important nuance of this scheme is that it focuses on Malaysian companies and enterprises. Foreign companies are not eligible to apply, although companies with foreign ownership stakes may; producer companies must be at least 51% Malaysian-held, and user companies 70% held. Malaysia may, and probably should, consider loosening this rule to encourage foreign participation in renewables.

Singapore

Singapore’s Green Plan features five pillars: City in Nature, Sustainable Living, Energy Reset, Green Economy, and Resilient Future. Each one involves incentives.

Characteristically, Singapore’s ambitions are not just around the greening of its own society but to be a hub for green finance for the region; to this end, it announced in its 2022 budget that the state would issue S$35bn (US$26bn) of green bonds by 2030 to fund public sector green infrastructure. The Monetary Authority of Singapore has a task force to make the city state an international financial centre for sustainability, and a new framework was published for sovereign green bonds in 2022.

Specific incentives include the S$180m (US$135m) Enterprise Sustainability Programme to support Singaporean companies, especially SMEs, in their sustainability journey. There is also an Energy Efficiency Fund to support businesses with industrial facilities, a Water Efficiency Fund to help manage water demand, and schemes for rooftop green energy, building retrofits and sustainable bonds.

Singapore aspires to be a regional hub for funds across all areas, certainly including renewables, and has worked to build an infrastructure and regulatory environment that supports their establishment.

Vietnam

Vietnam’s national strategy prioritises the investment and use of renewables in the development of its energy industry and sets policies on incentives and assistance.

Tax incentives cover all areas of renewables. They include a four-year initial tax holiday from the date of commercial operation, followed by a further nine to 15 years at a 10% preferential rate before the standard 20% corporate income tax rate kicks in. There are also exemptions on customs duties for five years on imported machinery, vehicles and raw materials, provided they are not available domestically.

Vietnam previously used a Feed-in Tariff (FiT) scheme to guarantee a fixed price for renewable energy producers. Since 2022, however, state utility EVN has switched to a negotiable selling price with an appropriate ceiling.

There are also incentives around land use fees and research funding.

For the future, Mini-Grid programmes could offer supplementary incentives for the installation of solar equipment on government buildings, such as schools or hospitals, particularly in rural areas.

Thailand

The Thai Board of Investment (BOI) offers investment incentives for renewable energy projects, including up to eight years of corporate income tax exemptions capped at the total invested amount before the usual 20% rate is mandated. There are also import duty exemptions for machinery and raw materials, an immigration fast track for foreign workers, and permission to own land.

A FiT scheme guarantees a fixed payment rate for renewable energy producers, setting a long-term power purchase agreement (PPA) for solar, wind and biomass over 25 years.

There are calls for a clearer FDI rule book. Restrictions on foreign shareholding and governance under the FiT scheme offset some of the BOI’s benefits and should be re-evaluated. The industry would also benefit from shifting the zoning model towards southern regions, allowing for more regional development.

It would also be useful to incentivise solar adoption at retail/individual household level to make it more accessible to a wider population, and to promote the Net Metering Programme, as is the case in Malaysia.

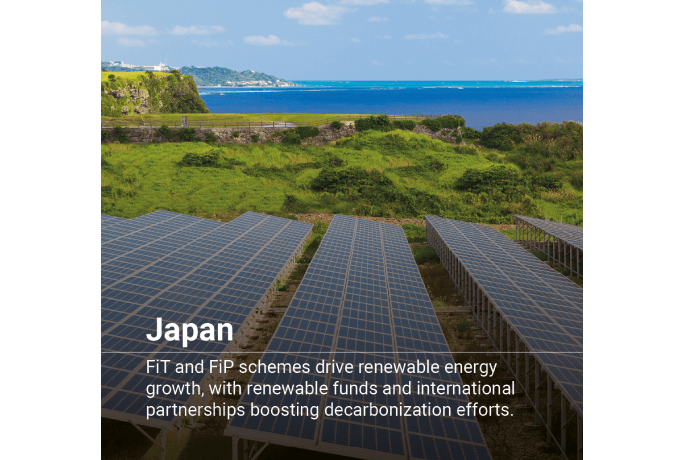

Japan

Japan’s FiT scheme began in 2012, obliging electricity utilities to buy renewable energy on fixed-term and fixed-price contracts. FiT auction-winning renewable energy generators secure investment incentives and have secured access to the grid. This has been most effective: according to Nomura Research, the share of renewable energy in Japan grew from 10% to 20% between 2012 and 2020.

This scheme has been refined with the Feed-in Premium (FiP) scheme, implemented in parallel from 2022. Here, the difference between the reference price and market price is paid to the FiP auction-winning renewable energy generators based on electricity sold in the wholesale market. The idea is to further mature the renewable energy market to reach government goals on the national electricity mix.

Several renewable funds have been established in Japan, investing both domestically and internationally. There have been discussions between US investment firms and Japanese trust banks to develop funds for Japanese decarbonisation efforts.

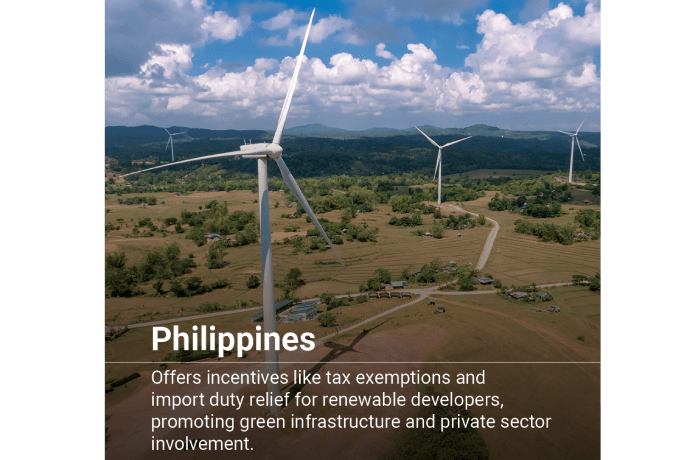

Philippines

Incentives in the Philippines date back to the Renewable Energy Act of 2008. Its provisions include a seven-year income tax exemption for renewable energy developers, duty relief on relevant imports, net operating loss carryovers, accelerated depreciation, VAT exemption and other incentives.

The Philippines has a strong track record of using both public funding and public-private partnerships to finance green infrastructure, including issuing sovereign green bonds, providing credit enhancement incentives and risk mitigation measures such as sovereign guarantees. The larger private sector groups, including Ayala Corporation and BPI, have invested in renewable assets.

However, there is scope for further incentives for the private sector, such as increased market commercialisation for renewable energy, and expansion of the credit enhancement and risk-sharing options the government provides.

Overall, the combination of incentives and a friendly regulatory environment on one side, and an asset class that is still difficult for the mainstream to access on the other, makes Asian renewables a compelling proposition for the funds industry.

How can TMF Group help?

We can provide detailed guidance and support on regulations around renewable energy investment in Asia. Contact us today.