GBCI 2022: Complexity in accounting and tax

TMF Group’s Global Business Complexity Index 2022 explores 292 different indicators relating to business complexity. Our analysis covers three core areas of business administration, and ultimately assigns an overall complexity score to each of the jurisdictions assessed.

This article focuses on the second of those three key areas of business: accounting and tax. Here we take a closer look at some of the findings from this year’s Global Business Complexity Index (GBCI), along with commentary from our subject matter experts.

Increased global alignment of accountancy and tax principles

A key factor that drives simplicity is the gradual global alignment of principles in the accountancy and tax worlds. In the long term, this has considerable benefits for international businesses as they have the advantage of being able to operate in a uniform manner across different jurisdictions and regions, which brings operational efficiencies. However, local nuances over how principles are applied can make a huge difference to complexity in any one jurisdiction.

The adjustment period following the adoption of new standards results in varying degrees of confusion and uncertainty. This can bring short-term complexity for businesses, as they adjust to meeting new globally mandated regulations and practices in certain jurisdictions, while in some locations the way in which general principles are adopted may be localised, meaning the changes affecting businesses can have a long-term effect.

The most significant upcoming move to standardise accounting and tax operations is the introduction of a minimum global corporation tax. Due to be introduced in 2023, the tax rate will be set at 15%. Its introduction is expected to be via a stepped approach, impacting large companies first and then medium sized. At this stage, it is still unclear how this will eventually be rolled out to smaller organisations. It is still too early to say whether some countries may choose to apply the changes to all corporate taxpayers, large and small, though they may be governed by OECD rules.

2022 will be remembered as the year when the global tax community committed to a significant change, the introduction of the minimum global tax rate.

The complexity caused by the introduction of this minimum global corporation tax rate will have the highest impact on jurisdictions that currently boast a particularly low or non-existent corporate income tax, such as the UAE. The significant tax advantages of setting up and operating in this jurisdiction have been the primary driver when it comes to attracting foreign businesses, so a global corporation tax regime would reduce the jurisdiction’s attractiveness. The UAE government has announced that it will introduce corporate income tax for the first time next year. This will be set at 10%, edging the UAE towards the forthcoming minimum global rate.

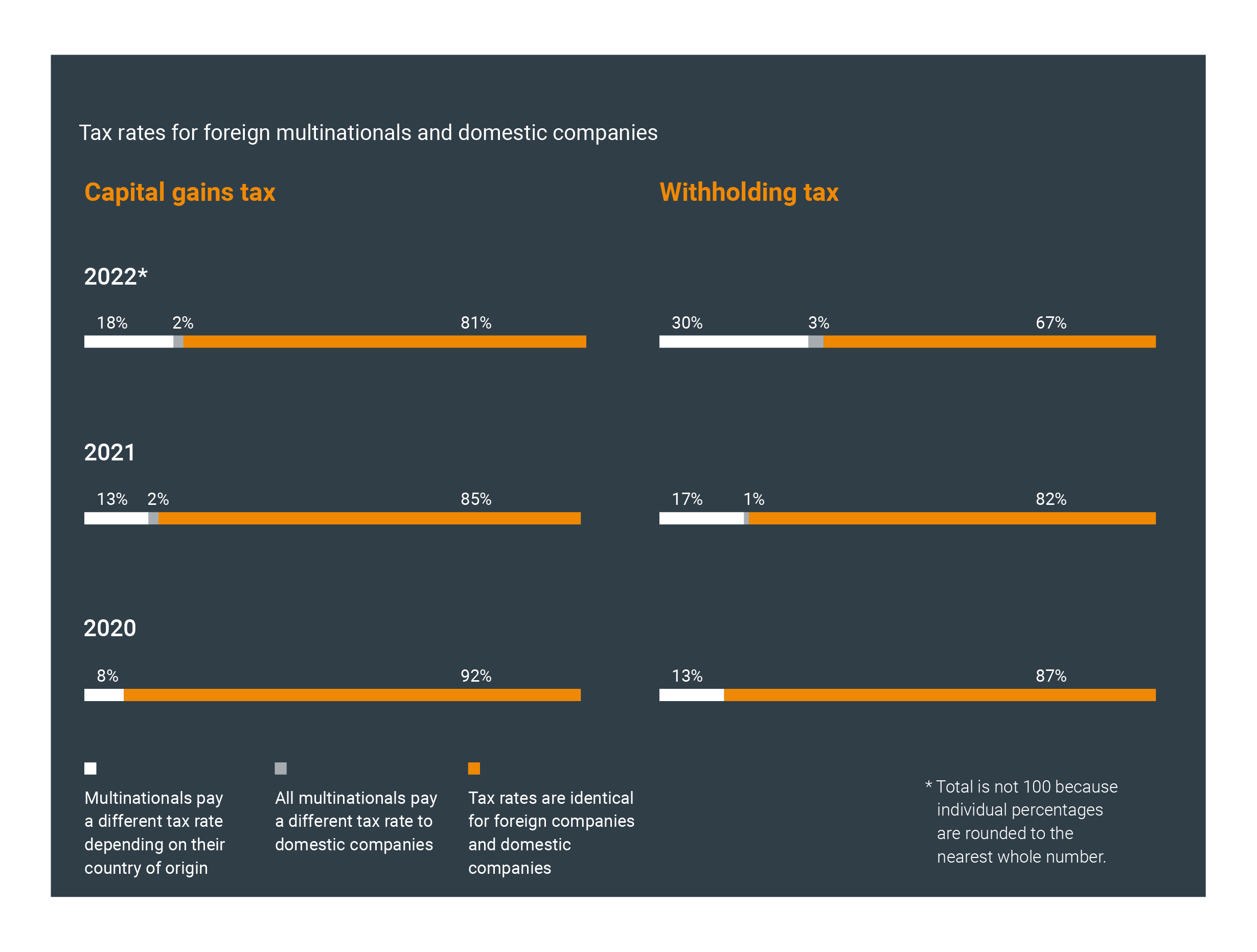

Standardisation can be observed at a jurisdictional level as well as globally. For instance, there is more alignment now between domestic and multinational businesses when it comes to paying capital gains and withholding tax.

Vietnam is following a similar trend after introducing social insurance contributions for expatriate employees on the 1 January 2022. This means that foreign workers and their employers will now be subject to the same social insurance requirements as domestic workers. While in the long term, such moves toward standardisation will make processes simpler through uniformity, in the short term, companies in Vietnam may face complexity as they adjust internal systems and processes to accommodate changes to social insurance contributions.

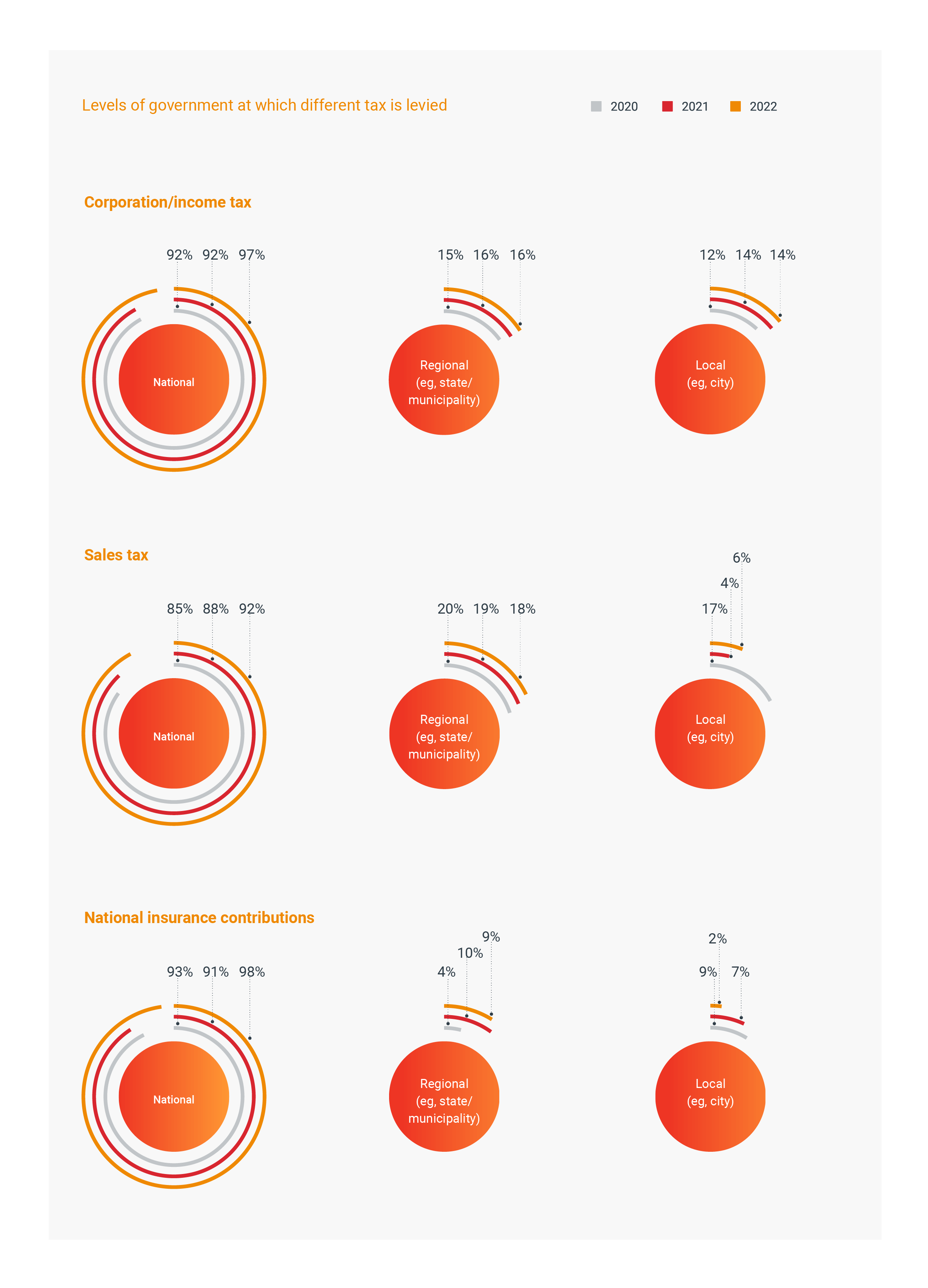

We see another shift towards standardisation when looking at the levels of government at which certain types of tax are levied. There has been a gradual shift to a more nationalised approach which, in turn, drives simplicity for businesses.

Despite this move towards a more standardised approach globally to paying tax at a jurisdictional level, countries such as the US, Brazil, and Colombia still levy tax at multiple levels, including by state. In Brazil, not only is there tax variation between different states and municipalities an organisation operates in, but also between business sectors. Brazil is also the jurisdiction that makes the highest number of changes to tax rates each year – a major factor in its position at the top of this year’s GBCI ranking.

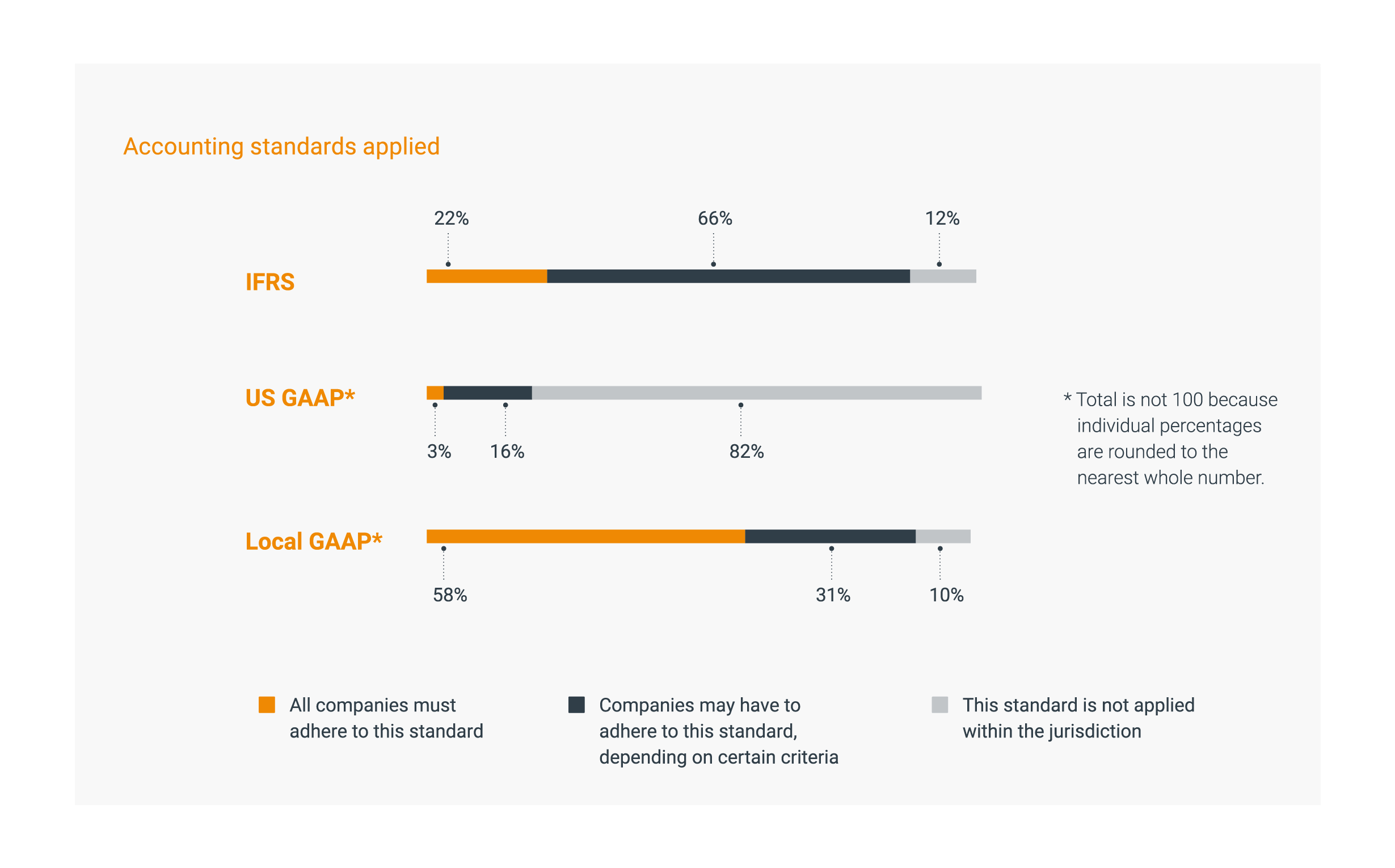

Another factor is a focus on greater alignment with international standards such as IFRS. In recent years there has been a global trend to better align with IFRS and international practice. Overall, this is viewed as a beneficial move for businesses as it serves to make local accounting practices easier to understand.

Local GAAP is still the most commonly applied accounting standard. However, local doesn’t necessarily mean localised, as we see in cases such as Italy. Since 2015, the Italian government has made a concerted effort to align with IFRS, despite having local GAAP in place. Therefore, even with certain local standards and practices remaining in place, an international approach to accounting and tax and global standardisation is still very much on the rise.

Governments stricter but also more supportive

Globally, governments are becoming stricter each year when enforcing tax rules and regulations. Authorities have focused on developing tax audit plans to identify tax risks in the economy and are focusing on auditing companies that operate in those areas.

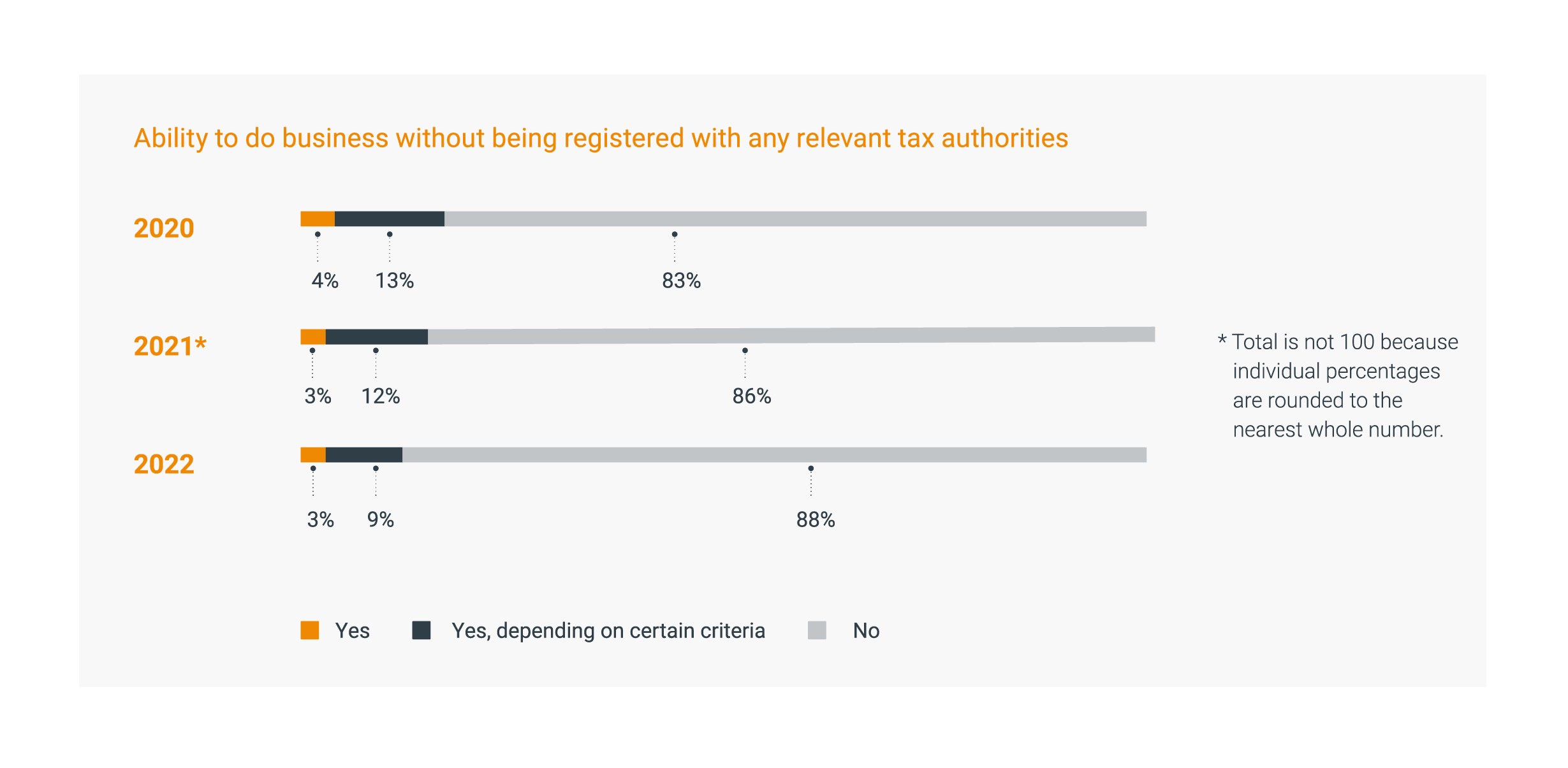

Since 2020, the number of jurisdictions that allow businesses to operate without being registered with tax authorities, either regardless of criteria or depending on certain criteria, has gradually decreased. Only 3% of jurisdictions now permit this, including the UAE and US, demonstrating a move towards a stricter approach to doing business.

Along with this move towards stricter tax governance, tax authorities are becoming more inclined to spend time with taxpayers to help them understand tax regulations. This is particularly the case in Europe, where tax authorities are running programmes for companies, aiming to help taxpayers with their understanding of tax regulations so that they remain compliant.

Companies will need to assess how the changes in tax policies impact their operations, cash flows and investment decisions.

This move towards being more supportive is a driver of simplicity, owing to the improved direct communication and collaboration with tax authorities. This aids companies by reducing the time and money that they could potentially end up spending on preventing or dealing with tax controversies.

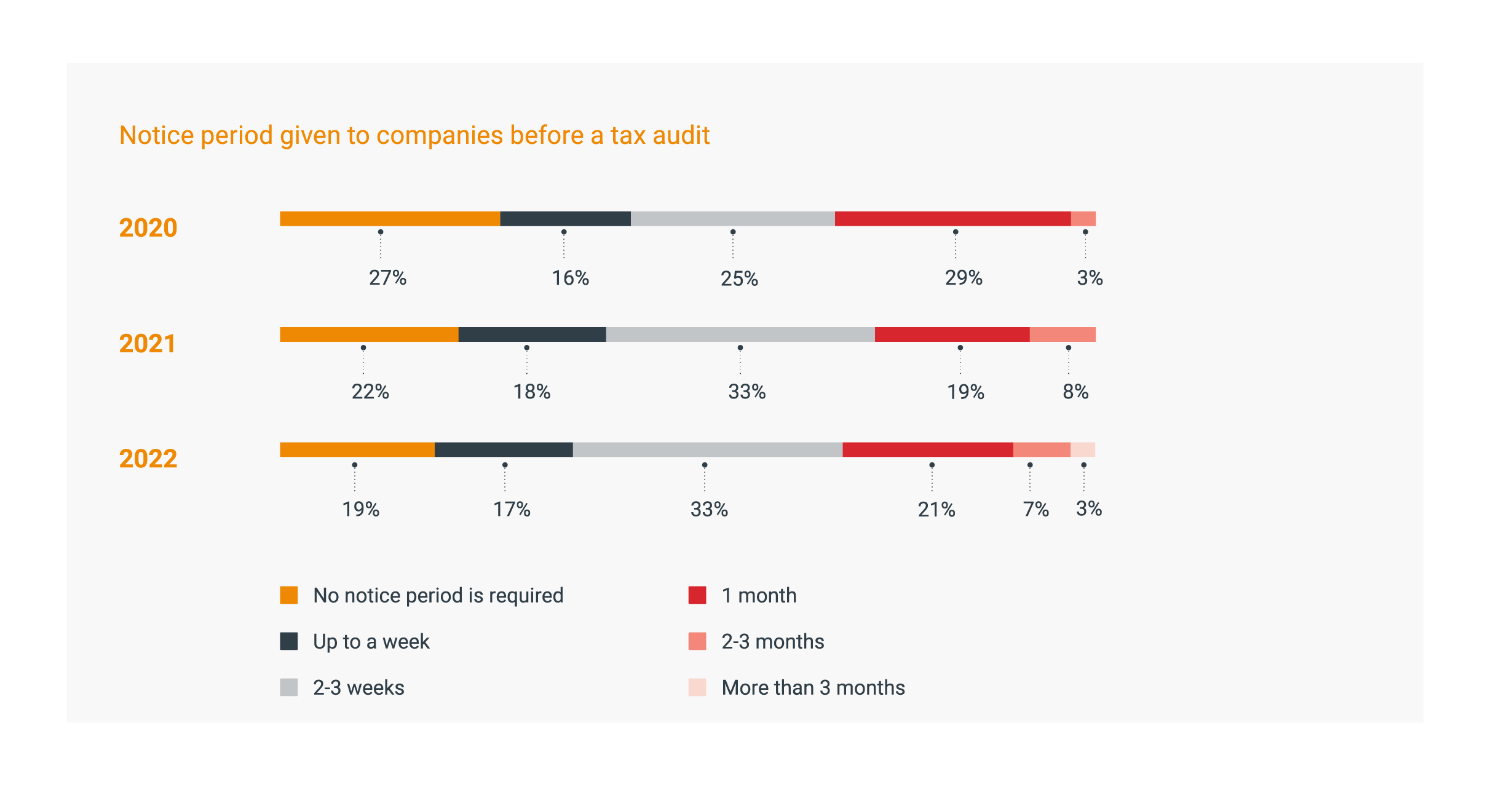

Another example of this move towards being more supportive or lenient, is that more notice is generally being given to businesses before a tax audit takes place. In 2020, 27% of jurisdictions reported that no notice was needed before a tax audit, a figure which has dropped to 19% in 2022. Giving more notice allows businesses to better prepare, so they are less likely to encounter issues during an audit.

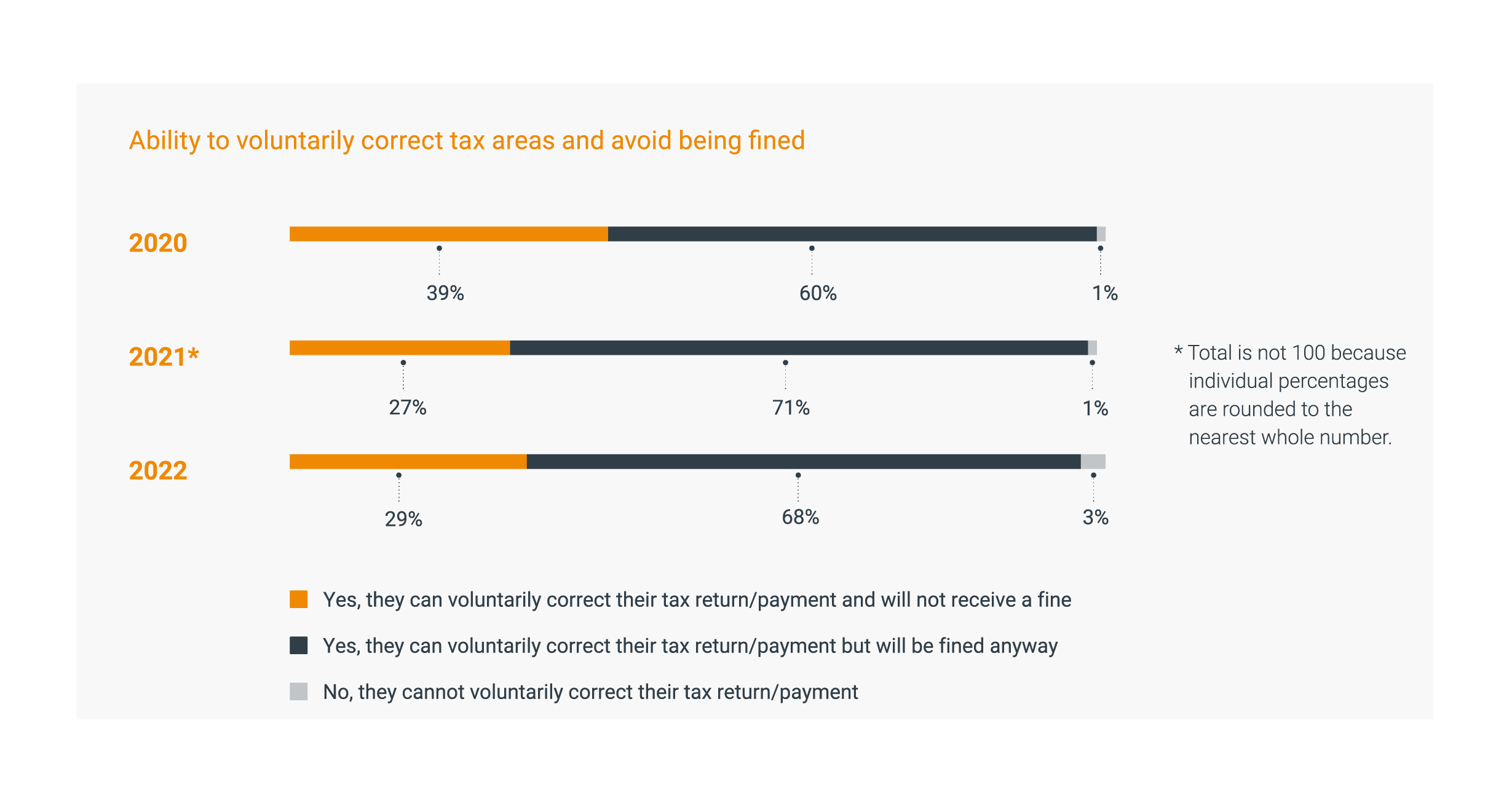

Similarly, the percentage of jurisdictions that allow companies to voluntarily correct their tax returns or payments without receiving a fine has increased since 2020. In 2022, it is still the case that most organisations will receive a fine even after voluntarily correcting their tax return, however there is a definite move towards greater leniency.

Digital approach to accounting and tax still on the rise

As well as the trends and developments above, the move towards digital solutions and reporting has continued. This has been spurred on by Covid-19, which limited the ability for face-to-face interaction and encouraged greater dependency on technology.

One example of this move towards digitalisation is in Poland, where electronic invoicing has been introduced. While this is optional for now, it will become compulsory in 2023. New digital reporting requirements can create challenges for organisations as they work to update existing processes or adopt new ones. Dataflows need to be redesigned and the impact on technology needs to be assessed and understood. Digital reporting and detailed transactional reporting require a certain level of technological enablement and so adequate investment and support is needed.

This is just a continuation of all the international efforts to make the tax systems more suitable for the digital age. The focus is on fair tax policies that will allow taxation where consumers are located and that will reduce the variations in tax rates.

Another trend involves jurisdictions beginning to exploit big data and artificial intelligence to conduct more data matching. With this, it becomes simpler to identify contradictions in tax data and address these through an audit. This can reduce complexity for governments themselves but can create additional burdens for organisations tasked with satisfying higher levels of scrutiny.

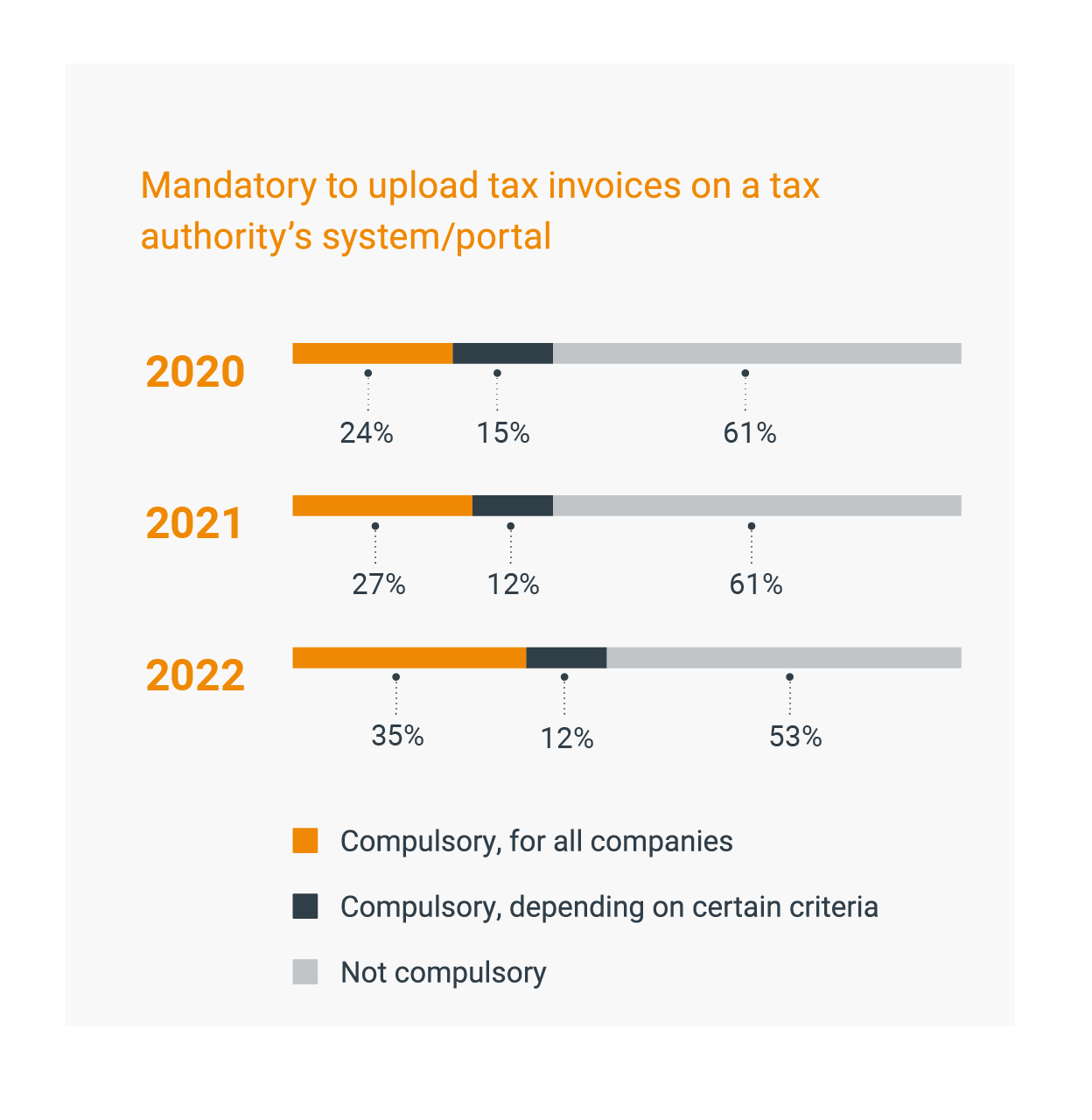

Globally, the compulsory uploading of tax invoices electronically via the authority’s system or portal is increasing. In 2020, it was compulsory in only 24% of jurisdictions for all companies to do this, but the figure has now risen to 35%. Serbia, for example, will begin transitioning to e-invoicing this year.

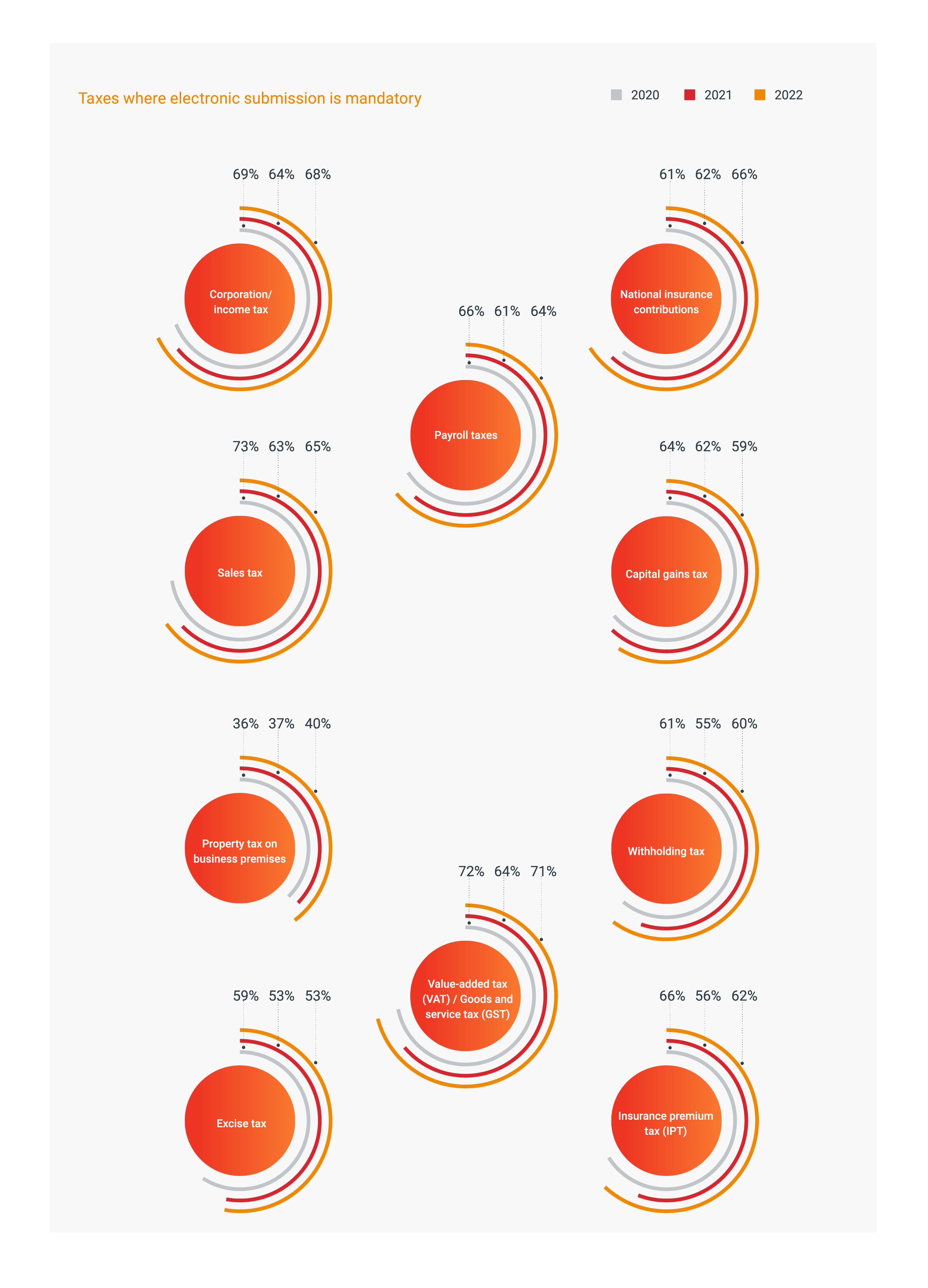

When we look at the mandatory electronic submission of taxes overall, it has remained on a par or is lower than in 2020. For example, the mandatory electronic submission of capital gains tax is less widespread in 2022 than it was in previous years. Conversely, national insurance contributions must be submitted electronically in more jurisdictions in 2022 than in 2020.

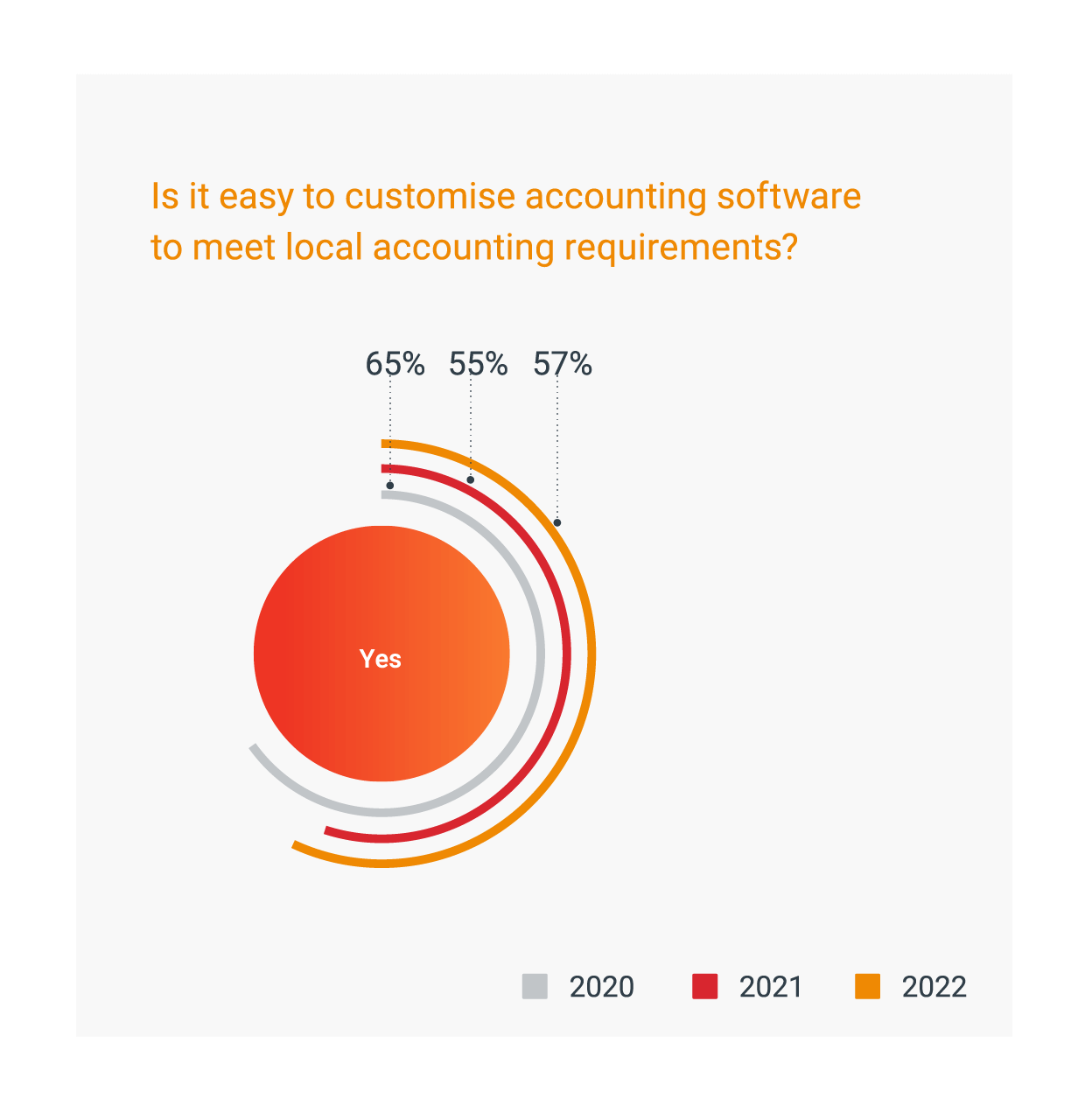

Our analysis has found that customising accounting software is difficult in more jurisdictions in 2022 than before Covid-19. In 2020, 65% of TMF Group experts globally agreed that it was easy to customise accounting software as per local accounting requirements, but this figure has dropped to 57% in 2022. In jurisdictions such as Greece and France businesses can face difficulty adapting their accounting software to local ways of working.

Global tax transformation: free webinar

To learn more about these shifts in the world of tax, why not sign up for our webinar at 2pm BST on 17 August 2022?

Global tax transformation – three rising trends CFOs should know about

Our tax experts will discuss the global alignment of standards, how governance is becoming stricter and the impacts of increasing digitalisation – and how tax teams can achieve success in this changing environment.

The Global Business Complexity Index

The GBCI 2022 provides an authoritative overview of the complexity of establishing and operating businesses around the world. It explores factors driving the success or failure of international business, with a focus on operating in foreign markets, and outlines key themes emerging globally as well as local intricacies across 77 jurisdictions.

Explore the GBCI rankings, analysis and global trends to help you find your path to growth, amid the complexity of corporate compliance.

To download and read the report in full, visit the Global Business Complexity Hub today.

To find out more about the drivers of business complexity in the jurisdictions that matter to you, why not explore our Complexity Insights Dashboard?