GBCI 2021 follow-up: Global compliance trends

In June, we published our annual Global Business Complexity Index (GBCI) report, providing an authoritative overview of the complexity of establishing and operating businesses around the world. Examining 292 indicators across legislation, compliance, accounting, tax, human resources and payroll, our report publishes a global ranking of 77 key jurisdictions based on the complexity of their business environments.

We focus specifically on global compliance trends. In line with the broader trend towards responsible governance outlined in the GBCI, we’ve observed increasing transparency requirements around the world. Increasingly, jurisdictions are requiring that companies appoint a certified accountant to manage their accounting and tax activities – and with this requirement in place, we’ve seen penalties for non-compliance becoming stricter. In addition to the research that contributed to this year’s GBCI, we have also overlayed GDP and FDI data from the World Bank onto our complexity index to uncover new insights such as attractiveness to outside investment and population prosperity.

Accounting standards are becoming increasingly localised

Looking first at accounting standards, we’ve observed a continuation of the battle between the aspirations of international norms and the maintenance of local standards. While global regulatory standards exist, local standards still dominate in this area. Local GAAP (Generally Accepted Accounting Principles) is applied to all companies in 57% of jurisdictions today (up from 42% last year). And concurrently we’ve seen the declining role of IFRS, from a quarter (25%) of jurisdictions using these standards in 2020, to only 19% today.

Transparency requirements are rising

The GBCI documented a trend towards responsible social governance, and this has been observed too in the realm of compliance. Companies are being subjected to increasing transparency requirements, with company information becoming ever more accessible to the general public, in a bid to combat malpractice by making it more difficult to exploit complex legal structures. For example, the requirement to provide UBO and/or PSC information to a central register has increased from 68% of jurisdictions requiring this in 2020, to 71% this year. More jurisdictions, including the US, are set to contribute to this trend in the near future.

Compliance timelines vary substantially

Key compliance timelines across jurisdictions can range from a few days to several months. To cite one example, in 22% of jurisdictions globally, local authorities do not have to give a notice period to carry out a tax audit. Yet in over a quarter (27%) of jurisdictions, companies must receive at least a month’s notice, and in some cases as much as three months.

Looking at incorporating a company, timelines can again vary significantly. Incorporation can take place in less than a week in 27% of jurisdictions globally, yet in a minority (9%) the incorporation process will exceed two months and could even last up to a year. In Taiwan, for instance, incorporation can take between four and six months due to the fact that many businesses require special licence approvals. Investment linked to Chinese funding must also adhere to special processes that take additional time to receive governmental approval.

The number of institutions involved in incorporation also varies from country to country. In one in three jurisdictions (35%) companies need only contact one institution, yet 36% of jurisdictions require at least four institutions to be notified. A poor appreciation of local rules and jurisdictional variations can lead to significant delays in establishing an entity.

Companies are increasingly required to appoint certified accountants

Alongside the localisation of accounting regulations and increasing transparency obligations, we’ve also observed governments moving to ensure that companies adhere to these standards. Globally, jurisdictions requiring entities to appoint and use certified accountants to assist with their accounting and tax compliance has increased. While these requirements still affect only a minority of jurisdictions, the year-on-year growth has been significant. In 27% of jurisdictions an entity must appoint and register a certified accountant with the authorities – this has grown from only 17% of jurisdictions in 2020. Similarly, 14% (compared with 8% last year) of jurisdictions require companies to appoint a certified accountant and register them with the local Chamber of Commerce.

Penalties for non-compliance are becoming stricter and personal liability has increased

The greater requirement to appoint certified accountants to ensure accounting and tax compliance may partly explain the penalties imposed for misdemeanours becoming stricter. In the case of inaccurate calculations for tax filings, while fines remain the most common penalty, other forms of punishment have become more prevalent globally. For example, the enforced suspension of business activity has increased from 13% of jurisdictions in 2020 to 25% today. In addition, we’ve seen an increase in the likelihood of licence suspension (from 9% in 2020 to 14% today) and outright prevention from doing business (8% in 2020 to 18% in 2021).

Company directors may be concerned that we've observed an increase in non-compliance leading to personal consequences, with personal liability even carrying the risk of imprisonment in some cases. In most jurisdictions, directors are personally liable for legal commitments (88%), tax compliance (81%) and shareholder damages (89%). Severe sentences (eg imprisonment) can be applied in around a third of jurisdictions for failure to register for tax (39%), or company secretary failings (28%). In a smaller proportion of jurisdictions, directors can even face severe sentences for inaccurate or late tax filings. This trend towards personal liability again supports the observed trend towards enforcing responsible governance.

GBCI 2021 in context

The GBCI reveals insights surrounding corporate compliance and the complexities of running a business around the world. However, to truly understand the gravity and meaning of the GBCI, it is important to consider the context in which it sits. Specifically, the economic, social, and political factors at play globally, and within each of the jurisdictions analysed.

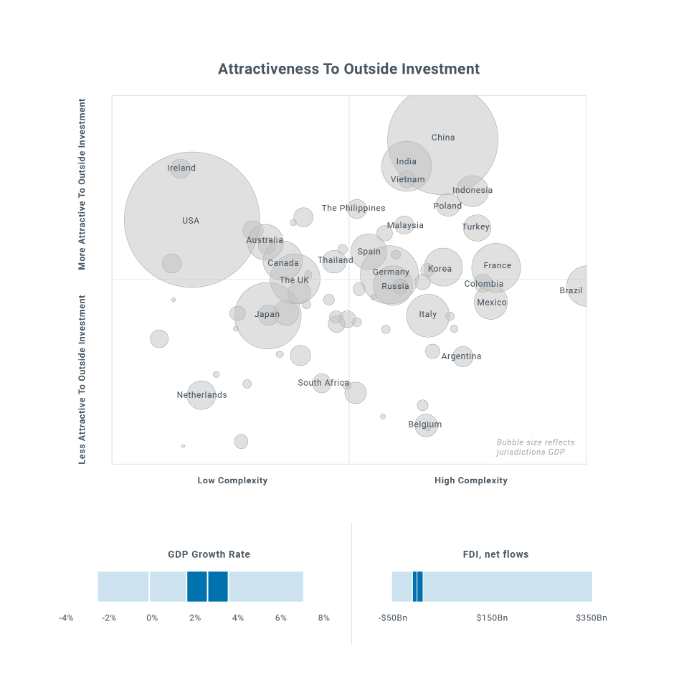

We’ve combined our GCBI insights with data from the World Bank, measuring GDP growth and net FDI flows, to better understand how attractiveness to invest in terms of financial prosperity collates with complexity.

Focusing on wealthier jurisdictions, the USA, for example, has a high GDP growth rate and net FDI flows, combined with a low ranking of 71st in the GBCI, making it a very attractive jurisdiction both in terms of financial opportunity and the simplicity of its business environment. It’s unsurprising, therefore, that the USA is a huge global business hub, and is home to some of the world’s largest commercial enterprises.

Another global giant in terms of financial opportunity, again with a high GDP growth rate and net FDI flows, is China. However, in contrast with the USA, this is a more complex jurisdiction to incorporate and operate in, ranking 12th in this year’s GBCI. Some of this complexity is driven by business restrictions imposed by the Chinese government relating to FDI, making incorporation more challenging in certain industries, particularly for entrants into this market from abroad.

However, where there is high complexity and attractiveness in terms of financial growth, there may be good opportunities for businesses. We’ve found that a significant number of financially attractive jurisdictions rank higher in the GBCI 2021, meaning that for those who can successfully navigate and manage the challenges of business complexity, the rewards can be significant.

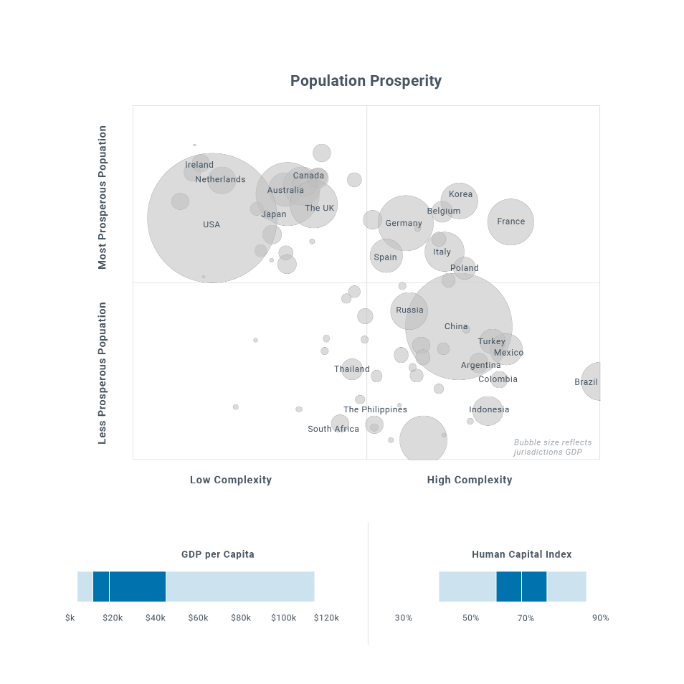

The simplest jurisdictions typically have the most prosperous populations

When focusing on the prosperity of the population in jurisdictions and complexity, we see that almost all low complexity jurisdictions have more prosperous populations. For instance, the Netherlands and the USA rank 70th and 71st respectively in this year’s GBCI; both have demonstrably prosperous populations. This suggests that there is potentially a link between simplifying an economy's business environment and the ability to build wealth and improve living standards.

The Netherlands in particular is widely regarded as a forward-thinking jurisdiction when it comes to ensuring a good standard of living and protection for its citizens. For example, all Dutch citizens are required to join a compulsory health insurance scheme that costs each person approximately €95-€120 per month. In 2016, the Euro Health Consumer Index ranked the Netherlands first for healthcare, validating the high standards in the jurisdiction.

Caution is key in certain jurisdictions due to risk of injustice and imprisonment

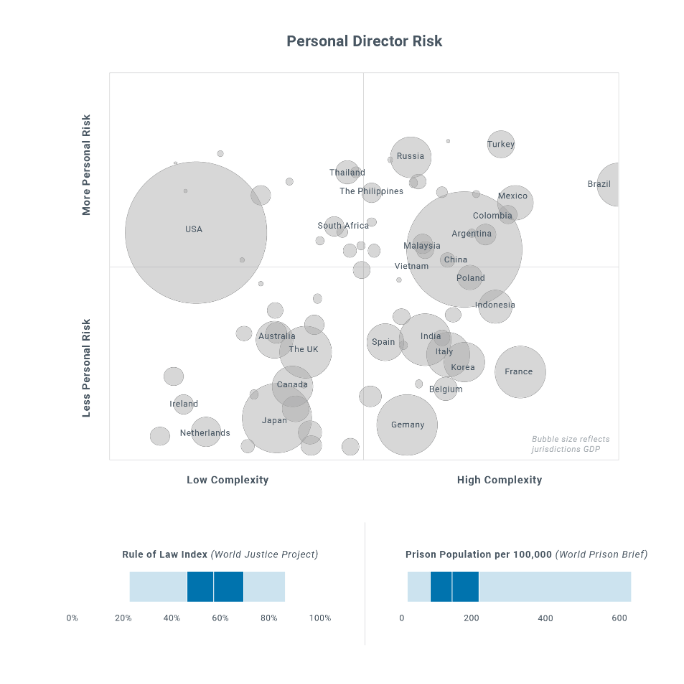

The final lens we can apply to the GBCI relates to injustice. The World Justice Project compares the fairness and integrity of judicial systems in its Rule of Law index, and the World Prison Brief collates proportional prison population data for each country. Combined, these indexes can offer a sense of the level of injustice risk that directors may face in a jurisdiction.

Jurisdictions with a complex business environment coupled with a high injustice risk will represent a greater concern for those with responsibility for entities. This is especially true if non-compliance can lead to punishments and directors can be held personally liable. Caution will need to be exercised when incorporating and operating in such jurisdictions.

Brazil, for example, ranks as the most complex place to do business in GBCI 2021, and is also a jurisdiction of concern for both personal risk and potential injustice. Brazil has faced high levels of uncertainty over the past year, concerning both the presidency of Jair Bolsonaro and his administration’s handling of the pandemic. According to Human Rights Watch, Bolsonaro has sought prison sentences for those who have criticised his handling of the Covid-19.

The Global Business Complexity Index 2021

As we have seen, compliance requirements are on the rise globally and penalties for misconduct are becoming stricter. It’s perhaps more important than ever before to operate in full compliance in order to avoid sanctions and other penalties linked to establishing and operating a business.

Complexity can raise the stakes of operating in certain jurisdictions, particularly in those with high injustice risk and high complexity, where the consequences of getting things wrong can ultimately be personal.

To help you to bring clarity to the complexities of doing business across borders, download your copy of the GBCI today.