How significant risk transfer is powering progress and unlocking capital efficiency

As credit markets evolve, the dynamic between banks and other lending institutions continues to change. The expanding significant risk transfers (SRTs) market supports increasingly complex and bespoke transactions that are transforming the way banks manage capital and credit risk.

As this market matures in European financial centres and gains regulatory acceptance while also picking up momentum in emerging global regions, investors should learn how to navigate this growing market sector.

Understanding significant risk transfer

Significant risk transfer (SRT), also known as credit risk transfer (CRT) in certain markets, represents a sophisticated approach to capital management for banks. By transferring a significant share of a portfolio’s credit risk to alternative investors, banks can better manage their risk-weighted asset (RWA) exposure while unlocking the potential to lower the capital reserves they hold.

This availability of capital allows banks to utilise their balance sheets while expanding their lending opportunities to energise economic growth. It is an innovative approach where banks can increase efficiency by diversifying their credit concentration risk and address both regional and sector-specific, cyclical or high-risk challenges without stifling their growth momentum.

For investors, SRT deals open the door to tailored, diverse loan portfolios with promising yield prospects, allowing them access to previously unavailable asset classes while being protected by vigilant regulations with extensive criteria that guard the integrity of the risk transfer process.

SRT frameworks

There are several different methods employed to carry out the transfers, but the underlying mechanics and ultimate objectives remain fundamentally similar.

In these structures, banks continue to hold the loans on their balance sheets while transferring the corresponding credit risk through synthetic securitisation, utilising mechanisms such as:

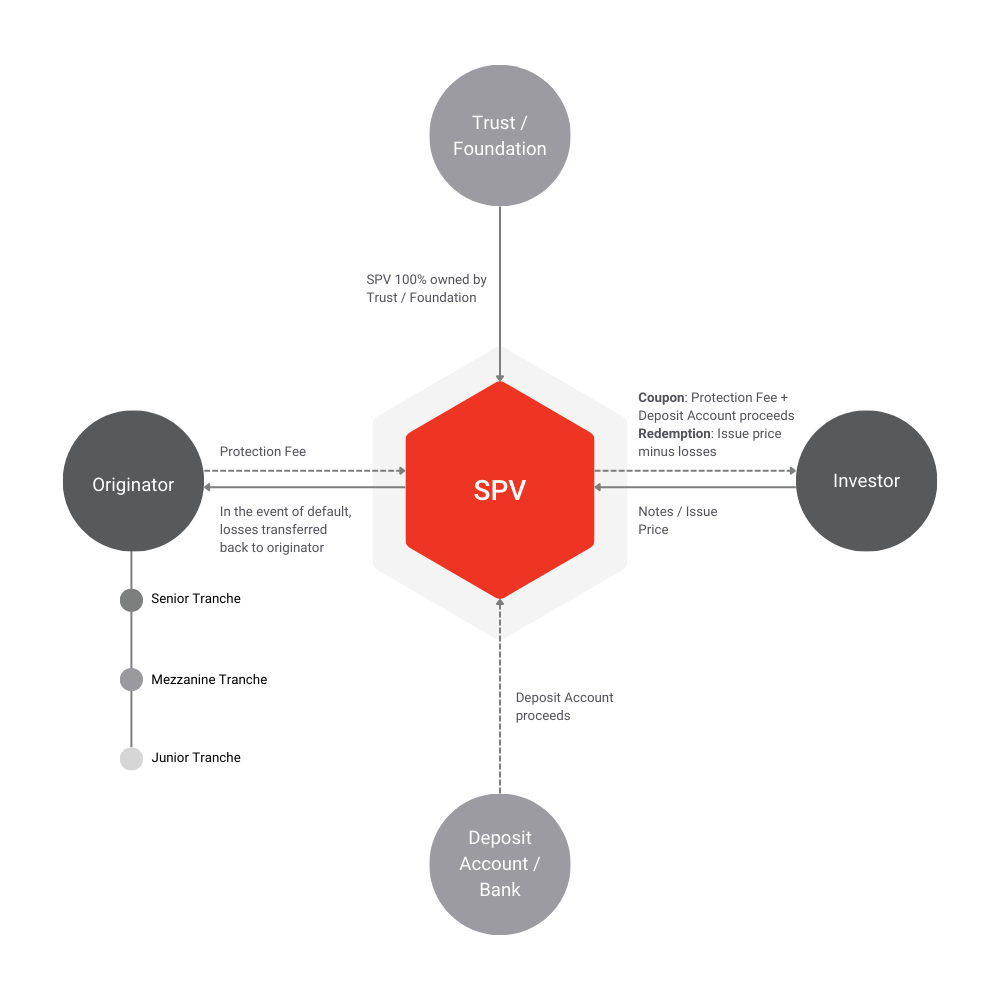

- Traditional securitisation (true sale) – involves the outright sale of loans to a special purpose vehicle (SPV), established at its core

- Synthetic securitisation – uses derivatives to replicate credit risk while retaining underlying assets

- Direct convertible loan note (CLN) – a funded instrument with conversion features linked to credit performance

- Risk-sharing agreement – an arrangement where losses above a set threshold are shared

- Credit default swap (CDS) – a derivative that transfers credit risk protection during a credit event

- Credit risk insurance – insurance that covers losses from credit defaults or adverse events

- Private / bespoke transactions – tailor-made risk transfer agreements structured to meet the unique requirements of the parties involved

Below is an illustrative example of a traditional securitisation (true sale) structure.

TMF Group’s role in the SRT space

SRT structures require sophisticated administration and multijurisdictional expertise to manage risk and stay compliant with the stringent regulations. This behind-the-scenes work is essential to make SRT and CRT deals possible.

Banks undertaking SRT deals often need to establish special purpose vehicles (SPVs), appoint trustees or agents to handle cash flows and collateral and ensure regulatory compliance across borders. As an administrator of these deals, TMF Group provides support at every step of the transaction lifecycle.

The typical roles of TMF Group in SRT transactions and their associated investor or financing structures include:

- SPV management – incorporating and administering issuer vehicles

- Facility and collateral agent – managing credit protection payments, holding and safeguarding collateral

- Cash manager – handling payments, premiums and loss settlements

- Trustee and security trustee – protecting the rights of both banks and investors

- Loan administration – the process of managing a loan from disbursement to repayment, ensuring compliance with terms, accurate record keeping and timely communication between lender and borrower

By taking on these independent and expert roles, TMF Group helps banks and investors participate in SRT deals with the confidence that the structure will be properly managed in compliance with local laws.

Banks can focus on the strategic and regulatory capital aspects while TMF Group handles the day-to-day administration, from coordinating payments to maintaining trust accounts and corporate records.

Corporate services providers like TMF Group are essential in the SRT market as neutral parties to manage special purpose entities and perform fiduciary duties. This independence and expertise are critical, given that SRT trades often involve private and bespoke arrangements that must satisfy stringent legal and reporting standards.

The future of SRT: trends and opportunities

As the SRT market continues to evolve, several important trends are emerging.

Regulatory focus

Regulatory compliance remains paramount for successful SRT execution. Europe leads the way with a mature and highly developed SRT market, shaped over two decades by regulatory milestones such as Basel II, CRR and evolving EBA guidelines.

These frameworks have created clear rules of engagement, driving the widespread use of SRT transactions for European banks seeking capital relief and risk optimisation. The adoption of SRT/CRT in other regions, particularly North America, is gathering pace, but remains at an earlier stage of development.

In the US and Canada, rising capital pressures, evolving regulation and lessons from the regional banking crisis of 2023 have sharpened interest in SRT transactions.

Transparency and data

The market is experiencing a shift towards greater transparency. Detailed data on the performance and structure of the reference portfolio must be shared with investors and regulators.

We see a push for greater transparency, as some SRT notes are now listed or reported, which helps investors perform due diligence and fosters a healthier market. Both issuers and investors benefit from clearer information on historical defaults, modelling assumptions and ongoing deal performance.

Structuring complexity

SRT transactions are bespoke and can be complex to negotiate. There is no one size fits all template - each deal must balance the bank’s objectives, the demand on investor risk/returns and regulatory restrictions. This means higher upfront structuring and legal costs. The complexity is worthwhile given the benefits, but it requires expertise and careful execution.

Talk to us

Our active involvement in this space, as evidenced by our growing portfolio of SRT deals across Europe and CRT deals in the US and emerging markets, has been key for banks executing capital relief trades.

Whether we’re acting as trustee on a synthetic securitisation or managing an SPV issuing credit-linked notes, we bring the operational know-how to support these innovative transactions.

To find out how our services can benefit your SRT deal, make an enquiry today.