Indian retailers should get ready for IFRS 16-driven change

In examining the likely impact of the standard locally, India’s vibrant but highly fragmented retail sector stands out.

Indian corporations, like their counterparts around the world, are working to ensure compliance with Ind AS 116 - the local equivalent of the IFRS 16 accounting rule - which is mandated by the Ministry of Corporate Affairs and came into effect in April 2019.1 In examining the likely impact of the standard, the country’s vibrant but highly fragmented retail sector stands out.

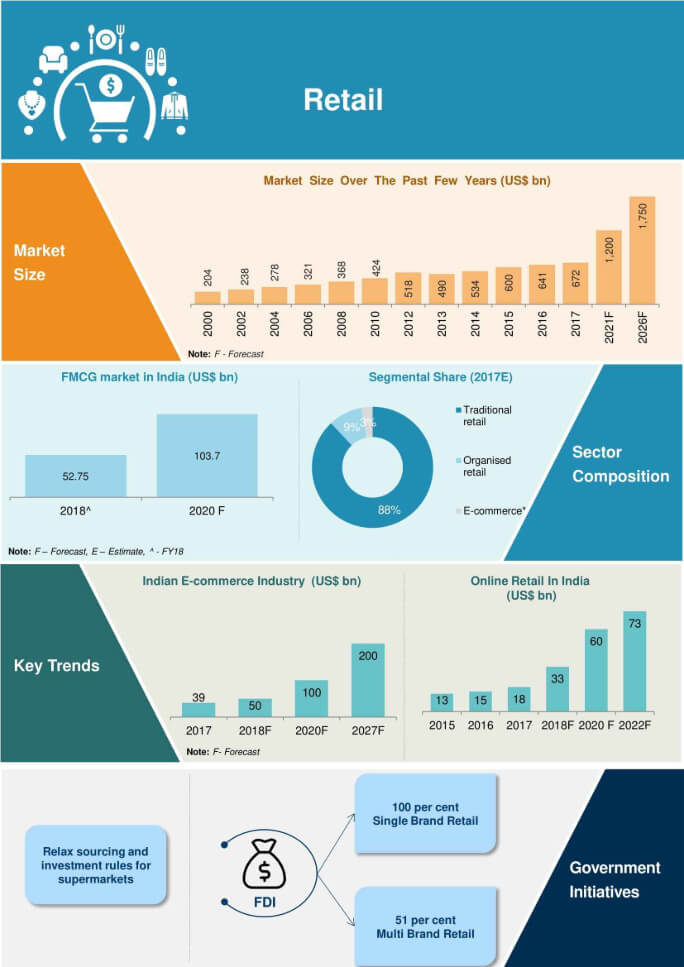

Source: India Brand Equity Foundation

The objective of Ind AS116, like IFRS 16, is to account for lease transactions in a way that allows users to transparently assess the amounts and timings of all cash flows, assets and liabilities arising from a lease.2 Naturally, the new standard is expected to have the most significant impact on the accounting departments of lessee corporations that manage a large number of leases. Globally, this means companies in the aviation, software, telecom and retail sectors - which typically tend to rely on operating leases - stand to be the most affected.

In India, the burden of complying with the new rule is likely to fall inordinately on companies in the country’s sprawling retail sector, which is highly dependent on rental properties. According to some estimates, the global retail industry will see a 98% median increase in debt from capitalising leases as required by IFRS 16.3

The top 10 major retailers in India operate thousands of stores while across India there are hundreds of smaller companies operating, at a conservative estimate, about 25 stores each. This means lease portfolios tend to be very large and geographically spread out, with agreements localised to suit state-specific laws.

The data consolidation challenge

Given this diversity, which is further complicated by varying lease payment schedules, one of the key challenges Indian retailers face is data-gathering. For instance, a retail company with its headquarters and centralised accounting operations in Mumbai, will have to deal with consolidating information on all the operating leases entered into by its local offices around the country.

This can be a significant undertaking given that most retailers have historically relied on accounting systems, processes and controls run on basic spreadsheet software - with the possible exception of the largest operators, who may have in-house enterprise resource planning (ERP) software and the capability to customise systems to accommodate the new lease accounting standard.

Recognising the limitations of their systems, small players have now begun to work with software developers – many of whom have sprung to life to serve this very need – to help them build accounting programmes that can handle the IFRS 16 standard. This is a positive development as it will equip these companies to gather, assess and manage data in a more systematic way, and make accounting decisions required by the new standard that will have a bearing not only on the companies’ books, but also possibly help enhance visibility on their overall operations.

Crunching numbers, Exercising judgment

Once a company’s accounting department has access to the consolidated lease information, the next challenge is for the systems to account for the changes in the treatment of leases. With IFRS 16 requiring that most leases, with few exceptions, be shown on company balance sheets, one primary issue concerns whether to account for a lease payment as a separate lease component or not.

A lessee might elect to apply the practical expedient of accounting - one of many available to make the transition to the new rule easier - for a lease and the associated non-lease component, treating it as a single lease component. If the practical expedient is applied, the cash flows associated with the non-lease component will increase the liability and right-of-use asset recognised on the balance sheet.

This is determined by asset class and companies are likely to consider the significance of the increase in relation to the effort and complexity of obtaining the necessary information to separately account for the lease and non-lease components. Retail and consumer lessees with material leases will need additional processes, controls and documentation to ensure appropriate and consistent application of the guidance. For example, the guidance requires an appropriate allocation based on relative stand-alone prices that maximises the use of observable prices.

This is crucial because while earlier both lease and non-lease components would be routed through the profit & loss (P&L) account as a single operating expense, the new standard provides an option to segregate assets from lease components. As a result, combining both will result in higher capitalisation of the asset and higher earnings before interest, tax, depreciation and amortization (EBITDA). But, at the same time, it will result in a higher lease liability on the balance sheet.

Companies also have to assess whether their accounting systems can handle the separation of variable payments that are not linked to a rate or index, and treat them as expenses through the P&L account. In contrast, the earlier accounting standard did not require such a separation.

Complications can also arise in determining the nature or existence of a lease in certain transactions where the original lessee sublets a property to another lessee, or the rented property is relocated and the original rental contract does not specify a physical location for the outlet - as with a portable stall or kiosk, for example.

Terminal leases also need to be differentiated from those carrying an option to renew under the new standard. While the old system did not treat such leases separately, a lessee now has to decide on a lease term in advance and whether to exercise an option to extend the lease in the future, as this will determine the present value of future lease payments and also how the asset is valued.

These issues highlight the accounting judgments involved in adhering to the new standard, as well as the potential long-term impacts these judgments may have on the overall business. This makes it all the more crucial that bookkeeping decisions are made based on comprehensive knowledge of Ind AS 116, and full awareness of its various strategic and operational implications.

Talk to us

At TMF Group, our goal is to keep you compliant with local tax and accounting obligations through the entire corporate lifecycle, from redefining internal functions to rapid expansion in new markets. Whether you need help with statutory bookkeeping, consolidated account preparation or international management reporting, we can manage your accounting processes across any jurisdiction without any conflict of interest. On IFRS 16, we are here to help you with the following.

- Transition assessment and compliance: our global team of in-house experts can assess your current and past reporting for IFRS 16 compliance and offer direct and indirect tax compliance support in liaison with relevant authorities for registration, returns, calculations and recovery.

- Accounting and reporting: we can help maintain your books and records in accordance with IFRS 16 accounting standards in multicurrency formats and meeting relevant accounting policies used for management reports (including IFRS 16, local GAAP).

Need more information? Contact us today.

Learn more about the broader impacts and the strategies businesses should adopt - download the free report.

This article was originally published by BusinessWorld and Indian Retailer.

1 https://www.businesstoday.in/top-story/government-notifies-new-accounting-standard-on-leases-effective-from-april-1/story/332744.html

2 https://www.ifrs.org/issued-standards/list-of-standards/ifrs-16-leases/

3 ttps://www.pwc.com/gx/en/audit-services/publications/assets/a-study-on-the-impact-of-lease-capitalisation.pdf