Renewable energy in Asia – policy and potential

Asian nations offer considerable scope for investment in renewable energy assets, underpinned by state-level ambitions to achieve carbon neutrality. In the first of a two-part series, we explain where six diverse Asian countries wish to go with renewables, and the assets that will help them to get there.

Asian renewable assets represent fertile ground for funds. The Asia Pacific region is expected to attract around 40% of total global investment in renewable energy capacity between now and 20501, with Southeast Asia the focus.

The region represents a perfect storm of renewable needs: population growth, rising demand, pressure on supply, abundant renewable resources and an increasingly supportive regulatory environment to attract funds.

Asia tends toward clearly articulated long-term planning, from five-year blocks to generational targets. Through these blueprints it is clear that renewable energy forms part of the ambitions of many Asian nations.

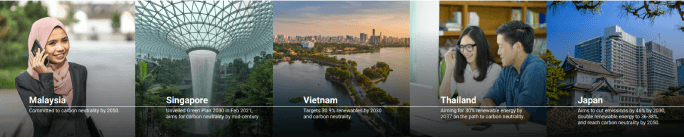

- Malaysia has committed to carbon neutrality by 2050. Its ambition is laid out in the Green Technology Master Plan Malaysia 2017-2030, and the Twelfth Malaysian Plan 2021-25.

- Singapore unveiled its Green Plan 2030 in February 2021. Intended as a whole-of-nation movement to advance a national agenda on sustainable development, the project is refined periodically, most recently in March 2022. Singapore aims to be carbon neutral around the middle of the century.

- Vietnam’s strategy on renewable energy to 2030, with a further vision to 2050, stems from a government plan published in 2015. Its Power Development Plan 8 calls for a minimum renewable energy goal of 30.9% by 2030 and 67.5% by 2050, with a goal being carbon neutrality.

- Thailand’s Renewable Portfolio Standard requires 30% of the country’s total energy consumption to come from renewables by 2037 (it is 16% today), on the way to being carbon neutral by 2050.

- Japan aims to cut greenhouse gas emissions by 46% by 2030 versus 2013 levels, It intends to do this by boosting renewable energy in its electricity mix to 36-38%, double 2019 levels. It has committed to carbon neutrality by 2050.

This political backdrop is extremely important in fostering a positive investment environment for funds to engage with renewables in Asia. It provides a spur for asset development and has prompted a host of incentives, explored in part two of this series.

The asset picture

The background to these ambitions is the compelling state of renewable assets in Asia. With just under 60% of the global population, more than half of global energy consumption, and as much as 85% of regional consumption sourced from fossil fuels today2, Asia both needs renewable energy and offers ample scope for project development.

Priorities vary: South Korea, for example, is a pioneering nation for offshore wind development, while India has conducted groundbreaking work in solar-powered irrigation.

Southeast Asian nations, given their tropical levels of sunlight, tend to tilt towards solar. In Thailand, for example, the Board of Investment approved 19 investment solar projects in 2022 with a total investment value of US$1.3 billion equivalent, followed by 12 wind power projects worth US$540 million. The Thai government wants 16,000MW of solar power by 2037, boosted by its ‘Adder’ programme, which encourages solar rooftop installations on government buildings.

Thailand

Thailand also has a mature hydropower sector, which is unlikely to grow significantly but has potential for refinement. For example, the world’s largest hydro-floating solar farm has been developed at the Sirindhorn Dam. Thailand also offers growth in biomass and wind.

Malaysia

Malaysia has potential across solar, wind, biomass, hydro, geothermal and tidal energy, but solar has been a standout. A technology called Net Energy Metering has been developed for solar PV systems, coupled with a solar leasing concept backed by the government.

Vietnam

In Vietnam, solar and wind are considered to have the greatest potential, with Vietnam’s 3,260km coastline an asset. All told, foreign direct investment (FDI) for renewable energy in Vietnam in 2022 amounted to US$5.46 billion. According to the Ministry of Industry and Trade that figure is equivalent to 56.1% of all renewable investments. Wind follows with 20.4%.

Philippines

In the Philippines, where there is a very strong track record of public-private sector partnership, hydro power has been the dominant renewable sector. To date, 352 of the country’s 645 grid-use renewable projects awarded by the government have been in the hydro space. Solar, geothermal, wind and biomass are also active. Biofuel and ocean energy projects are less widespread but have been successfully rolled out.

Singapore

Singapore lacks the space for widespread renewable rollouts of technologies like wind farms, but is prioritising solar, energy storage systems and smart grids. Short of available land, Singapore has become creative in finding places for solar deployment: examples include temporary vacant land and even bodies of water. Smart grids fit with the city state’s reputation for digital efficiency and innovation, allowing more diverse sources of renewable energy to be used while ensuring grid stability.

Japan

Japan, an island nation, has great potential for offshore wind, and the government is to run a series of public tenders. The first of these auctions was conducted in late 2022, while bids for the second round were due in June 2023. 10GW of capacity is already identified for upcoming auctions, part of a plan to increase capacity from 5GW in 2021 to 23GW by 2030.

As with the rest of the region, solar is dominant in Japan, accounting for 75% of renewable energy sources in 2021. The target here is 111GW by 2030, up from 66GW in 2021.

Crucially, in all of these countries there is a need for private sector investment alongside state-directed backing. Additionally, in an evolving environment, it is challenging for investors to back individual energy assets directly, creating a potent environment for funds to step in and create vehicles to link investment demand with operating assets.

So, Asia has two things that matter for renewable investment: a clear need, and a pattern of asset development. In part two of this article, we explain the technical incentives they are employing to attract funds.

How can TMF Group help?

We can provide detailed guidance and support on regulations around renewable energy investment in Asia. Contact us today.